The January 2021 Presidential Election Winners: President Pence and Vice President Harris?

October 2020

No, the general election on November 3rd will not be postponed, but the future President of the United States may be elected by a different group of voters on a much later date – and it may happen after the new Congress convenes on or around January 3rd. This election may be as close as it is disputed, and given the complexities and vagaries of election laws, the House of Representatives could very well elect the next President.

Several scenarios provide for this possibility. Since 538 Electoral College votes exist, the winner must secure 270 of them – a majority – to win the election. The 2000 Bush-Gore election illustrates just how close this election may be: Bush won with only 271 votes (to Gore’s 266).

For those adding together that election’s votes, one will notice only 537 Electoral College votes were submitted. One elector (from a state won by Gore) abstained. It is the first time an elector abstained, but not the first time one has refused to vote for the candidate for whom they pledged their vote (an action known as being a “faithless elector”). Absent a third-party candidate, the existence and actions of faithless electors represent one of two possible scenarios by which an election could fail to produce a majority winner.1

The other possibility would be the failure of a state’s votes to be counted since they lack certification. Understanding either scenario requires a review of the Electoral College process as governed by the Constitution and state and federal law.1 2

Before the general election, electors for the Electoral College are chosen by each state for each candidate. Under a typical, two-party election, at least two “slates” of electors exist – each one consisting of electors pledged to vote for a particular party’s candidate. After the election, each state mandates its own processes to verify the integrity and completeness of the election. For example, certain canvassing (similar to auditing) procedures take place. Each state has its own procedures and timelines.3

The problem arises in the fairly short timeline between the general election and the Constitutionally mandated new terms for President and Vice President beginning at noon on January 20th. According to federal law, the electors must meet and cast their ballots (in their respective states) 41 days after the general election (or December 14th for this year). It is these ballots that are sent to Congress for the official tally taking place on January 5th. In order to avoid any controversy about the legitimacy of the votes, a “safe harbor” period exists under federal law: if the slate of electors is certified by the state six days before the electors meet (or December 8th for this year), the slate is considered “conclusive” and will not be disputed in Congress.

If the “safe harbor” timeline is not met, both houses of Congress determine which slate of electors will be recognized from a state. This almost happened in the 2000 election. Many misremember the Supreme Court as “deciding the election” in favor of George Bush. In reality, Florida’s slate of electors pledged to Bush was to be selected (certified by its Secretary of State) when various lawsuits culminated in a Florida Supreme Court ruling to recount the ballots in four counties and all ballots throughout the state which did not select a Presidential candidate (under the assumption this was done in error). Such measures would have been physically impossible before the expiration of the “safe harbor” period, and Congress would have decided the issue (for which the only precedent, the 1876 Tilden-Hayes election, offers little guidance). The U.S. Supreme Court ruled the recount unconstitutional for various reasons and thus allowed Florida to certify its results in time to meet the “safe harbor” provision (actually, on the last possible day). Presumably, if Congress cannot resolve the matter, the electoral votes may simply not be counted (thus preventing a majority winner).

In another scenario, all of the states’ electoral results may be certified, but a faithless elector may not honor the majority vote from their state. There are 33 states (as well as the District of Columbia) that have laws compelling (e.g., via the threat of fines, removal from office, etc.) electors to honor their pledge. These laws were recently upheld as constitutional by the unanimous Supreme Court decision in Chiafolo v. Washington (concerning the 2016 election).4 Therefore, 17 states, including the swing states of Pennsylvania, grant electors the ability to vote their conscience. Other states, including swing states like Ohio, Florida, and Wisconsin, have laws against faithless electors, but still, allow the vote to be counted as cast. While a faithless elector has never impacted an election, a Republican’s discomfort with an “outsider” like Trump or a Democrat’s concern about Biden’s cognitive ability probably heightens the likelihood of wayward votes (or abstentions).5

What happens on January 6th if, according to the official reading of the electors’ votes, neither candidate secures a majority? According to the 20th Amendment to the Constitution, the House of Representatives “immediately” elects the President and the Senate elects the Vice President.

Such a scenario seems to suggest a President Biden and Vice President Pence (assuming the political control of Congress remains the same). But two nuances imply a different, or at least uncertain, outcome.

First, the House does not vote in the same manner as it does with matters of law or procedure (with each Representative casting one vote). Rather, each state casts one vote as determined by a majority of their Representatives. If such a vote was taken today and cast along party lines, Republicans would control the outcome by a vote of 26 to 23 (as Pennsylvania’s Representatives are equally split and Michigan, assuming Libertarian party member Justin Amash does not squash his disdain for President Trump, would vote Democrat – otherwise the vote would be 26 to 22).6

Second, the circumstances dictating this scenario’s result may not exist since the new Congress based upon November’s general election is sworn in on January 3rd. A change to a mere two states could swing the election in the House to Democratic control.

And what if the House of Representatives is deadlocked in a tie? Who becomes President on inauguration day? Vice President Pence would assume the Presidency. As the Senate can only vote for the two Vice Presidential candidates receiving the most votes (Pence and Harris) and since one cannot hold both offices, Kamala Harris would become Vice President by default.

President Pence and Vice President Harris. The acrimonious political landscape of the next four years may supersede that of 2020. Just another risk the financial markets have yet to consider.

Endnotes:

Maskell, Jack and Rybicki, Elizabeth. “Counting Elector Votes: An Overview of Procedures at the Joint Session, Including Objections by Members of Congress” Congressional Research Service. https://crsreports.congress.gov/product/pdf/RL/RL32717/12

CASEY: When did you first see the potential in cryptocurrencies, and what in particular did you find so compelling?

JOHNSON: I first started looking at cryptocurrencies back in the second half of 2013. We were watching what was going on with the banking crisis in Cypress. In December of that month, our founder and CEO, Patrick Byrne, made kind of an off-handed comment to a reporter saying: “we’ll start accepting cryptocurrency sometime in the second half of 2014.” That created a lot of buzz both outside and inside the company. We then had a group of developers approach management saying: “we should get this done more quickly, there’s no reason to wait six-to-eight months.” So, during the following weekend, a couple of teams of developers locked themselves in a room and started working on this project. On January 9, 2014, Overstock.com became the first billion-dollar retailer to accept bitcoin or any cryptocurrency. We like it for lots of reasons. We like it because it’s not a government-issued fiat currency which can be printed ad nauseum. We like it because it makes it easier for customers to buy things on Overstock.com’s website. We like it because we think it promotes freedom. I guess that last one is ultimately the best reason for bitcoin and other cryptocurrencies.

ROSENBERG: I was involved with cryptography and currency prior to bitcoin by over a decade, so I’ve been interested, but I finally really started paying attention to bitcoin in 2010. I saw this as just a brilliant combination of peer-to-peer networking and cryptography: the way they are doing hashes and proof of work and essentially making timestamp chunks of data which we call blockchain. I saw how this establishes trust between people who don’t know or trust each other. I thought: “wait a minute, this is a big deal.” So, I knew from 2011 or so that it was looking very promising. But you never truly know if these things are going to catch on.

RENTMEESTER: We first became aware of bitcoin in 2011 and found it to be an interesting free-market movement as a store-of-value and payment system outside of traditional banking. This was against the backdrop of a world that had come out of the financial crisis of 2008 by printing massive amounts of fiat currency to bail out Wall Street and the banks, taking on huge debt to do so. It seemed like a grass-roots uprising or “people’s money” fighting against our debt-based monetary system. In 2013, we began to better understand the true revolutionary nature of blockchain technology behind bitcoin and began to talk to investors about the potential for cryptocurrencies in a portfolio. This new system takes control away from central banks and governments, who are overspending and printing money carelessly, and gives power back to individuals. With bitcoin, you don’t need banks as a middleman and transactions can occur anywhere at a low cost. As former President Obama correctly described it, it was like a “Swiss bank account in your pocket.” From an investment perspective, we saw cryptocurrencies as potentially offering investors a very unique spectrum of outcomes. On one hand, it was a play on the upside of a new and disruptive technology: blockchain. On the other hand, it could possibly represent a hedge against a dangerously indebted global financial system.

CASEY: What, if anything, has surprised you about the growth in cryptocurrencies and their use over the last several years?

RENTMEESTER: Like many technological trends, it initially progressed slower than we would have thought at the time, but is now accelerating faster. It took people a long time to understand the disruptive nature of blockchain technology. They had to wait and see it proven by bitcoin as the prime mover and it’s now nine-years old. This was phase one of the rise in cryptocurrencies. Phase two is likely to be driven by liquidity and money entering this space. Since many, but not all, cryptocurrencies like bitcoin have limited supply, a big influx of capital is likely to drive prices higher. Phase three may well be an Internet-like crash followed by phase four, a building out of concepts in every industry disrupting incumbent industry leaders with blockchain solutions.

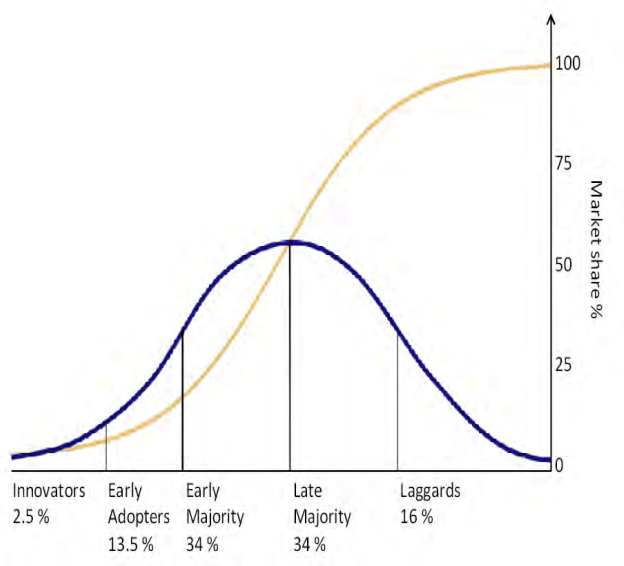

In hindsight, cryptocurrencies and blockchain technology are following a traditional technology adoption curve. In 1995, there were an estimated 16 million Internet users worldwide, representing less than 0.5% of the global population.1 Today, there are an estimated 20 million bitcoin wallets with at least $1, but only an estimated eight million wallets with $100 of more.2 This represents less than 0.5% of the global population and appears to us to be at a very similar juncture to where the Internet was in the mid-1990’s. Therefore, we are very early in this story. That said, we expect this cycle to be quicker than the Internet wave as recent technology adoption curves have been much quicker with a scalable technology.

ROSENBERG: The thing that pleased me and in fact surprised me were the number of people who became involved. All of a sudden, there were hundreds, then thousands of people who were really into this thing. Where did they come from? No one really has the numbers on this, but I bet you there are easily a hundred thousand people involved right now. Maybe two or three hundred thousand, who get up every morning and are trying to do something with cryptocurrencies. To me, the technology is really important, but even more important is this active, involved, and large group of motivated people.

JOHNSON: After we first started accepting bitcoin, there was obviously an initial surge of interest and a lot of crypto-bugs and enthusiasts were purchasing things on Overstock.com. Then it fell off to a fairly steady, small state of people using bitcoin to buy stuff on Overstock.com. But in 2017, we saw a steady increase in our cryptocurrency revenue. So much so that last summer we went from just accepting bitcoin to now accepting about 50 different cryptocurrencies. I guess what I would say is most surprising is that other retailers and service providers have been slow to accept cryptocurrency. For us, it made sense. We’re in the business of making it easy for customers to purchase goods from us. If they want to do is with American Express or PayPal or bitcoin, we’re going to accommodate them. I’m surprised that other retailers haven’t followed suit. Particularly during 2017 when cryptocurrencies have become all the buzz and all the rage. Last week there was an article on the front page of the Wall Street Journal. It said: “even your grandma cares about cryptocurrency.” Well if grandmas care about cryptocurrency, we think service providers and retailers ought to be accepting it.

CASEY: As an early adopter of bitcoin, how did that lead you to explore blockchain technology in general?

JOHNSON: It wasn’t soon after we began accepting bitcoin at Overstock.com that we realized that bitcoin is just the first killer application of blockchain technology. Underlying blockchain technology is really valuable. Email was the first killer app on the Internet, but the Internet became so much more than just a tool for delivering email. It now permeates our lives in so many ways. We think blockchain technology will be the same. What the Internet did for the transfer of information, we think blockchain technology will do for the transfer of value or assets. Back in 2014, we put together a division called Medici – now formalized as a wholly owned subsidiary of Overstock.com called Medici Ventures – which is investing in companies that advance blockchain technology. Today, we are principally focused on five different industries: capital markets, money and banking, property and land, voting, and identity. We think that in each of those industries people are transferring an asset; whether that’s their vote, a stock certificate, or some kind of property right – and it should be transferred through blockchain technology.

CASEY: Would you mind highlighting two or three of those underlying portfolio companies? What are they doing in their respective spaces and how disruptive they may be to their industries?

JOHNSON: We’ve invested in a company called Bitt which is working to bank the unbanked and the underbanked by providing a digital wallet while working with the Caribbean central banks. Today in the Caribbean, roughly 40% of the population is unbanked. That’s not because they don’t have jobs, or they don’t have an address, or they’re not paying utility bills – they’re doing all three of those things. But the banking regulations have become so strict that many people around the world are simply shut out of the banking economy. It is difficult for a cash-only citizen of the world to transact. A digital wallet dealing in a digital currency helps solve this issue. Given that cell phone penetration is around 140% in the Caribbean, it’s a place for the unbanked to store money and gain access to digital currency.

Another is in the capital markets area and it’s called tZERO. Typically, when people are buying and selling stocks or bonds, that transaction settles three days after the trade, or what the industry calls T+3. But with blockchain technology, people can buy and sell stocks, buy and sell bonds, and have the trade be the settlement. So, you get rid of your broker, the prime broker, the depository trust and clearing corporation, etc. Part of what we think is so great about blockchain technology is it eliminates middlemen. Middlemen are by definition inefficient and rent-seeking. They add time, they add cost, and they add the opportunity for fraud in a transaction. We have them in place because, historically, we’ve needed them to allow people who don’t know each other to engage in commerce. Blockchain provides trust through technology. You and I, whether we know each other or not, can now trust each other because blockchain technology says that we can. That’s a great way to do two things: eliminate inefficient middlemen and re-humanize commerce so that you and I, through an electronic handshake, can do business person-to-person. We really think the re-humanization of commerce is something that’s a social good of blockchain.

We have another one called Factom that’s doing something both in banking and in land. It’s working with big banks which are issuing mortgages to help them ease their compliance burden through blockchain technology. The volume of mortgages on a dollar basis issued today versus right before the 2008 crisis is about the same, but the compliance costs for those mortgages have skyrocketed. Factom’s view is if mortgage banks can put all of that paperwork on blockchain, then it’s easily auditable and it can’t be changed. The compliance costs go way down, lessening friction, and making the cost of accessing capital much easier. It’s blockchain technology helping the average person. What we see going forward is that blockchain technology is going to begin affecting each of us. We may not know how or when it’s being used, just like we don’t always know how and when the Internet is being used, but we know it makes our life easier and we know it makes it better. It will be with same with blockchain.

CASEY: How well do you think the current cryptocurrencies are working? That is, are the various forks proving they work or do you see them as a negative?

ROSENBERG: I do see problems with it. Not that it’s going to destroy anything, but it’s just that some of it is pretty juvenile. There are particular people who were in bitcoin really early and who are very rich as a result. To their credit, they’re keeping very active in the community and sponsoring new things and helping people. They are doing what’s basically the right thing. But some of these guys are battling for their version of what bitcoin should be, and they are getting very emotionally involved in it. And the beauty of bitcoin, the incredible thing about bitcoin, is that it’s surviving its enemies and it’s surviving its friends. And it’s surviving them very well. So, the forking doesn’t bother me from a general standpoint. If you like your way better, then it should be fine – split off and prove your better way – but don’t get into big arguments.

RENTMEESTER: Overall, they are working extremely well given that this was simply an idea back in 2008. The bitcoin blockchain has never been hacked or compromised to our knowledge, making it one of the most secure methods for storing and transmitting information in the world. Sure, there are growing pains, with network congestion as demand accelerates beyond the current ability to handle it. Again, this reminds us of the early days of the Internet when it could take 30 seconds to download a webpage. Those issues will resolve themselves now as they did then. In many ways, this is the most important free-market experiment in the world. Can a peer-to-peer system function and adapt without a centralized middleman, corporation, or CEO running things? So far, the answer appears to be “yes.” That is why I see forks, or splits of a blockchain, as a positive. Those that didn’t like bitcoin’s path split off to Bitcoin Cash and Bitcoin Gold. It’s pure capitalism – almost like natural selection – may the best fork win.

CASEY: What future applications of cryptocurrencies do you foresee which have yet to be fully developed?

RENTMEESTER: The Initial Coin Offering phenomenon is allowing whole new business models to spring up almost overnight as challengers to incumbents in almost every industry. ICOs represent the chosen path of raising money for many tech entrepreneurs using blockchain versus a traditional Wall Street fundraising approach. In fact, ICOs raised an estimated $3.6 billion in 2017 according to Coinschedule. Thus, the first disruption is the old way of fundraising that Wall Street has controlled for so long. Along those same lines, stock markets may be disrupted. There is a wave of decentralized exchanges in cryptocurrencies that don’t have centralized exchange providers taking fees, instead allowing investors to trade shares directly with other investors, or “wallet to wallet,” in a decentralized exchange.

However, the applications go well beyond banking and Wall Street. Imagine a world where all sensitive private data transmits through the blockchain. Such as securing identities on the blockchain or transferring secure medical records. Or a world where people without a banking account can use cryptocurrencies to process micro- transactions made possible by the ability to transact at low costs in fractions of a dollar. Or social media sites where value-added content providers and users own the system and are directly compensated instead of corporations like Facebook and Google.

We are entering a global peer-to-peer world where we will interact with others without the need to pay a middleman to secure trust. That was Satoshi Nakamoto’s key premise when he launched bitcoin – to build a “trustless” system. Suffice it to say that we believe blockchain technology will impact almost every human on the planet.

ROSENBERG: Well, there’s a couple of things that spring to mind. The first thing that hasn’t been quite solved yet is replacing credit cards systems. I think credit card systems today process about fifty or sixty thousand transactions per second. Bitcoin can’t do that. It just won’t. Now I have been hearing stories of other new cryptocurrencies that are designed differently and are approaching Visa-type speed right now. So that’s a big area, if that works as well as they are saying it does, because all of a sudden, we’ll have a technology that can compete with Visa and Mastercard. Now Visa and Mastercard have immense inertia and a lot of people are making a lot of money with it. Every time you use your credit card, Visa gets two or three percent. That’s sixty thousand transactions per minute. That’s a lot of money. They have immense market share, so cryptocurrencies not going to take them over right away, but they will eventually. If cryptocurrencies reach comparable speeds, then it’s simply a better way to transact: you don’t have to pay these high fees and if you’re a merchant, you don’t have to deal with charge backs. It’s simply a better way to do it.

It’s amazing how many different niches have applicability for cryptocurrencies. For example, I read about one which was working on dental insurance. You buy your token and then you buy them in advance or trade for them however you like, and then a token is good for one third of a root canal, or for three fillings, it you takes two tokens to buy a bridge or whatever it is, but they’ve got this, and it’s kind of a replacement for dental insurance.

You get your tokens and they’re good for dentistry for anybody in this network. You can just cash your tokens in and get the dental work you need. Right now, if you can get dental insurance, it is very expensive. These guys are solving the problem. There’s all kinds of things that you can do with these new tokens. People are using them for giveaways for business similar to how people used to give away coupons for something. The other area that I think is really interesting, but it’s still in development to an extent, is smart contracts, Ethereum in particular. This is a really interesting idea, it actually came out in the early 1990’s. You set it up and the contract executes itself. There are immense areas of application in business: you could automate certain businesses or you could automate departments inside of businesses. This is a really a big deal.

JOHNSON: Voting is a very promising area. When I think of all the times I’ve voted in an election in my life, I’ve never known for sure that my vote was counted as cast. There’s no way to verify that. I rely on a lot of trust institutions between my casting the vote, and it being counted. If you’re living in an area like me where you vote by mail, then you trust the county clerk to get you a ballot. You trust the county clerk to send the ballot to the right people. You trust the post office to get you the ballot and return it to the country clerk after you fill it out. You trust the county clerk to record that vote as a secret ballot – that is, without looking to see that it was you. You expect the voting machine to read it as you’ve cast it. That’s too many trust institutions and not enough knowledge for the voter. We think blockchain technology will allow people to vote remotely, by phone, perhaps using biometrics for identity confirmation. I can then confirm that my vote was counted for the person for whom I cast it. We think this has tremendous ability to increase participation in voting and to increase trust in our elected officials and institutions. It could really be monumental, particularly as voting participation has been on the decline. It’s time we reverse that pendulum and get going the other way.

CASEY: What is the greatest risk to the growth and value of cryptocurrencies?

RENTMEESTER: Government regulation is number one. However, we’ve long said that you can’t kill cryptocurrencies unless all world governments work to simultaneously ban them. That is to say, if you ban them in China, they prosper in the U.S. Kill them in the U.S. and they thrive in South America. Since there is no central location to cryptocurrencies, you can’t simply kill them in one country, fine a company, or fire a CEO. You are dealing with millions of decentralized users that make up the network. Any country turning their back on cryptocurrencies will soon find that they are lagging behind in technology in this key area.

Another risk is that with so many ICOs, there will be plenty of investment scams which could scare investors away. It truly is the Wild West out there. Expect more regulatory measures in the year ahead.

ROSENBERG: I agree that the negative repercussions of investment scams or heists are a risk, but I think this is lessening. There used to be nothing but negative stories on bitcoin. Now only half of them are negative. The real potential problem is regulatory. You always have to worry what the government is going to do. Although cryptocurrencies are not to their benefit, the reaction has been a bit mixed at the moment. For example, Japan has embraced them to an extent. I’m under no impression that regulatory agencies are ever going to be friends to the cryptocurrency community, but I certainly don’t want them to be our enemies. I’d rather they just left us alone. But maybe we’ve seen the worst of it.

The only thing that could really be a problem is if somebody could break the encryption, which is at this point really, really doubtful. The difference in difficulty between encrypting and decrypting is something like two to the one-hundredth power. I mean, engineers fight about this number, but let’s just say it’s somewhere in that range which approximates the number of molecules in the universe. So, I’m not too worried about it even with quantum computing. I mean we already have quantum-computing proof encryption, so we would just adapt the cryptocurrency program.

JOHNSON: The biggest risk is overregulation. When I think of humanity’s ability to adapt to new technology, the biggest boat anchor has always been overregulation. When I visit Washington, I’m frequently asked by agencies and staffers in Congress: “how do we get jurisdiction over bitcoin or how do we get jurisdiction over blockchain technology?” They want jurisdiction, in my mind, for one reason: to regulate. One of the reasons that the Internet flourished as much as it did and has was that, in 1996, President Clinton signed a telecommunications law which allowed the Internet to grow free and unfettered from state and federal regulation. I think we need to do the same with blockchain.

CASEY: What do you think is needed for cryptocurrencies to go mainstream?

RENTMEESTER: We are likely entering what’s known as the Early Adopter Stage in 2018. Less than 0.5% of the world’s population are in cryptos today, but we expect 2018 to be a transformative year where businesses and investors alike clamor to get involved. This stage is a key stepping stone toward mainstream adoption.3

We already hit a feverish pace in the second half of 2017 with governments, companies, and public figures discussing it. Of course, some were wildly in favor with others suggesting it was a fad or scam. Again, to us, it is very reminiscent of the early days of the Internet. Back then, many perceived the Internet to little more than a college chat room for techies with little real-life applicability. Two decades later, the Internet changed how the world communicates and shares information. We see cryptocurrencies and blockchain as a similarly powerful force which enables a new era of a global, peer-to-peer economy. This peer-to-peer nature means the middleman is no longer needed. They’ll be essentially extinct. We expect massive disruption in almost every major industry with middlemen.

3 Rogers, Everett (16 August 2003). Diffusion ofInnovations, 5th Edition. Simon and Schuster

Disclosures

All content and matters discussed are for information purposes only. Opinions expressed by Christopher Casey and Brett Rentmeester are solely those of WindRock Wealth Management LLC, a Registered Investment Advisor (RIA), and our staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. All activities of CryptoX Advisory are directed by WindRock Wealth Management LLC doing business as CryptoX Advisory.

Fee-based investment advisory services are offered by WindRock Wealth Management LLC, an SEC-Registered Investment Advisor. The presence of the information contained herein shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services.

Cryptocurrencies are a new and unproven investment, are largely unregulated, and may have account or “wallet” security issues or other technical computer concerns that impact an investment. Cryptocurrencies are an extremely volatile investment category that could lose all of their value. Specific investments and securities mentioned by WindRock Wealth Management personnel may be owned personally or for the benefit of said personnel and/or clients of WindRock Wealth Managmemt.

WindRock Wealth Management personnel may have a material interest in some or all of the investment topics discussed. Nothing should be interpreted to state or imply that past results are an indication of future performance. There are no warranties, expresses or implied, as to accuracy, completeness or results obtained from any information contained herein. The presence of the information contained herein shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services except, where applicable, in states where we are registered or where an exemption or exclusion from such registration exists.