This article was originally published by The Human Events Group on July 3, 2014

We have proposed a system for electronic transactions without relying on trust. – Satoshi Nakamoto, 20091

With this fairly mundane comment, the person or persons known as Satoshi Nakamoto (the jury is still be out) introduced bitcoin to the world. Since then, bitcoin has attracted widespread attention and interest – as well as numerous critics. Ironically, some of its most vocal detractors, such as Austrian economist Frank Shostak and financial commentator Peter Schiff, are champions of gold. As fiat currencies (money which exists solely due to the force of law, i.e., by fiat) further decline in value, will investors increasingly embrace a cryptocurrency such as bitcoin, or will they revert to the historically tried-and-true precious metals? Will it be bitcoin or gold?

As the values of bitcoin and gold are primarily contingent on their future acceptance as money, answering the question “bitcoin or gold” requires an examination of a more basic inquiry: what is money? Money is a medium of exchange and, as such, presupposes the ability to act as a store of value. Over two thousand years ago, Aristotle noted the primary qualities exhibited by money:

Portability

Durability

Homogeneity, and

Divisibility.

Money should also, at least before becoming accepted as money, possess “alternative value.” This term is unfortunately sometimes referred to as “intrinsic” value (as nothing possesses value without demand, nothing is intrinsically valuable).2 Gold, (and to a lesser extent silver) possesses these qualities and was therefore used as money until quite recently (1971). Bitcoin critics who are proponents of gold cite its lack of alternative value as a fatal flaw.

But is it? True, unlike gold or silver, bitcoin cannot be used for a non-monetary purpose. Perhaps this is not a weakness, but rather a strength. As bitcoin lacks physical form, it lacks alternative value, but herein lies its unique attribute relative to gold – there is nothing to physically transmit. In the characteristic of portability, it easily exceeds gold’s virtues.

Does this mean that bitcoin is no different than any fiat money which can be transferred with a computer keystroke? No, as its usage derives from general acceptance, not mandate.

And unlike the experience of all fiat currencies throughout time, bitcoin is limited in quantity (it is designed so only 21 million bitcoins can ever be “mined” into existence). Nakamoto remarked that in creating bitcoin he had removed trust. But more accurately, he removed faith and fortified trust, for just as gold and silver use nature (their elemental physical characteristics) as an objective standard, so bitcoin utilizes math (cryptography).

The question of what ultimately may be the future of money may be “bitcoin or gold?”, but perhaps the answer should be bitcoin and gold. For millennia, gold and silver coexisted as money, so why not bitcoin as well? Bitcoin is so unique in the history of money, and so complementary to gold, that one day in the future, it – or some other cryptocurrency (assuming they survive government regulation and financial repression) – may become more than today’s speculative investment.

2 For a real life example of the importance of “alternative value” as a quality of money, see “Only Criminals Use Honest Money” by Christopher Casey as published by the Mises Institute. <https://mises.org/library/only-criminals-use- honest-money>.

About the Author:Christopher P. Casey is a Managing Director with WindRock Wealth Management. Mr. Casey advises clients on their investment portfolios in today’s world of significant economic and financial intervention. He can be reached at 312-650- 9602 or chris.casey@windrockwealth.com.

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high net worth individuals, family offices, foundations and retirement plans.

All content and matters discussed are for information purposes only. Opinions expressed are solely those of WindRock Wealth Management LLC and our staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Fee-based investment advisory services are offered by WindRock Wealth Management LLC, an SEC-Registered Investment Advisor. The presence of the information contained herein shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services except, where applicable, in states where we are registered or where an exemption or exclusion from such registration exists. WindRock Wealth Management may have a material interest in some or all of the investment topics discussed. Nothing should be interpreted to state or imply that past results are an indication of future performance. There are no warranties, expresses or implied, as to accuracy, completeness or results obtained from any information contained herein. You may not modify this content for any other purposes without express written consent.

The fear of deflation serves as the theoretical justification of every inflationary action taken by the Federal Reserve and central banks around the world. It is why the Federal Reserve targets a price inflation rate of 2 percent, and not 0 percent. It is in large part why the Federal Reserve has more than quadrupled the money supply since August 2008. And it is, remarkably, a great myth, for there is nothing inherently dangerous or damaging about deflation.

Deflation is feared not only by the followers of Milton Friedman (those from the so-called Monetarist or Chicago School of economics), but by Keynesian economists as well. Leading Keynesian Paul Krugman, in a 2010 New York Times article titled “Why Deflation is Bad,” cited deflation as the cause of falling aggregate demand since “when people expect falling prices, they become less willing to spend, and in particular less willing to borrow.”1

Presumably, he believes this delay in spending lasts in perpetuity. But we know from experience that, even in the face of falling prices, individuals and businesses will still, at some point, purchase the good or service in question. Consumption cannot be forever forgone. We see this every day in the computer/electronics industry: the value of using an iPhone over the next six months is worth more than the savings in delaying its purchase.

Another common argument in the defamation of deflation concerns profits. With falling prices, how can businesses earn any as profit margins are squeezed? But profit margins by definition result from both sale prices and costs. If costs — which are after all prices themselves — also fall by the same magnitude (and there is no reason why they would not), profits are unaffected.

If deflation impacts neither aggregate demand nor profits, how does it cause recessions? It does not. Examining any recessionary period subsequent to the Great Depression would lead one to this conclusion.

In addition, the American economic experience during the nineteenth century is even more telling. Twice, while experiencing sustained and significant economic growth, the American economy “endured”

deflationary periods of 50 percent.2But what of the “statistical proof” offered in Friedman’s A Monetary History

of the United States? A more robust study has been completed by several Federal Reserve economists who found:

… the only episode in which we find evidence of a link between deflation and depression is the Great Depression (1929-34). We find virtually no evidence of such a link in any other period. … What is striking is that nearly 90% of the episodes with deflation did not have depression. In a broad historical context, beyond the Great Depression, the notion that deflation and depression are linked virtually disappears.3

If deflation does not cause recessions (or depressions as they were known prior to World War II), what does? And why was it so prominently featured during the Great Depression? According to economists of the Austrian School of economics, recessions share the same source: artificial inflation of the money supply. The ensuing “malinvestment” caused by synthetically lowered interest rates is revealed when interest rates resort to their natural level as determined by the supply and demand of savings.

In the resultant recession, if fractional-reserve-based loans are defaulted or repaid, if a central bank contracts the money supply, and/or if the demand for money rises significantly, deflation may occur. More frequently, however, as central bankers frantically expand the money supply at the onset of a recession, inflation (or at least no deflation) will be experienced. So deflation, a sometime symptom, has been unjustly maligned as a recessionary source.

But today’s central bankers do not share this belief. In 2002, Ben Bernanke opined that “sustained deflation can be highly destructive to a modern economy and should be strongly resisted.”4The current Federal Reserve chair, Janet Yellen, shares his concerns:

… it is conceivable that this very low inflation could turn into outright deflation. Worse still, if deflation were to intensify, we could find ourselves in a devastating spiral in which prices fall at an ever-faster pace and economic activity sinks more and more.5

Now unmoored from any gold standard constraints and burdened with massive government debt, in any possible scenario pitting the spectre of deflation against the ravages of inflation, the biases and phobias of central bankers will choose the latter. This choice is as inevitable as it will be devastating.

Endnotes:

Krugman, Paul. “Why is Deflation Bad?” [2] The Conscience of a Liberal. The New York Times 2 August 2010.

McCusker, John J. “How Much Is That in Real Money?: A Historical Price Index for Use as a Deflator of Money Values in the Economy of the United States.” Proceedings of the American Antiquarian Society, Volume 101, Part 2, October 1991,pp. 297–373.

Atkeson, Andrew and Kehoe, Patrick. Federal Reserve Bank of Minneapolis. Deflation and Depression: Is There an Empirical Link? January 2004.

The Federal Reserve is not currently forecasting a recession. – Ben Bernanke, Januuary 10, 2008 [1]

With Ben Bernanke’s exit as Chairman of the Federal Reserve, every political physician will opine on his legacy. Many will view him as the savior of capitalism. The others will agree, but caveat the compliment by stating his monetary mischief eventually exceeded its necessity. So while some may debate recent Federal Reserve policy, all condone his reaction to the Great Recession of 2008. His legacy will be viewed as having acted promptly, properly, and aggressively to the greatest economic threat since the Great Depression, for quantitative easing and negligible interest rates are universally proclaimed to have stabilized the economy and set the stage for future growth. This author disagrees.

Determining what Bernanke’s Federal Reserve should have done in a recession – and whether or not Bernanke acted properly – requires an examination of what causes recessions. Just as doctors can only properly treat patients with an understanding of germ theory, economists can only restore economic health through an understanding of business cycle theory. All cures require the cognizance of causality.

Bernanke has always been portrayed as an “expert” on the Great Depression, so surely he must understand the true cause of business cycles. In 2002, he clearly stated he knew the origin of recessions (or at least deep recessions, a.k.a. depressions) and believed them relegated to history, never to return:

I would like to say to Milton [Friedman] and Anna [Schwartz]: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again. [2]

What did the Federal Reserve do that Bernanke swore would never be repeated? What was this transgression it committed in causing the Great Depression? Bernanke, and all “monetarist” economists, blame the central bank’s contraction of the money supply. But clearly this did not cause the 2008 Great Recession, for none of the monetary metrics ever decreased. Faced with such facts, the Chairman of the Federal Reserve could reach one of two conclusions: either the 2008 Great Recession (and possibly all other recessions) had some different cause or causes relative to the Great Depression (which is nonsensical), or the monetarist theory of business cycles was in error. Bernanke chose the former. He chose unwisely.

Is there a better explanation of the business cycle? One which describes all recessions and depressions? One which explains the widespread and severely erroneous judgment of businesses in forecasting the future as revealed in the “bust”? One which illustrates why it is a cycle, and why this cycle first appeared in the 19th century? One which justifies why capital goods industries are more sensitive to booms and busts relative to consumer goods industries? One which explicates why significant money supply expansion precedes every single recession?

The Austrian school of economics has such an explanation. When a central bank increases the money supply with fiat currency, it artificially decreases interest rates. As interest rates are a universal market signal to all businesses, investments which previously appeared unprofitable now seem to make economic sense. However, these expenditures are actually being “malinvested” relative to the natural level of interest rates as determined by the supply and demand of savings.

When a central bank ceases or severely mitigates its expansion of the money supply, the natural level of interest rates reasserts itself, and a recession ensues. Recessions are the beneficial period by which previous investment wastes and errors are corrected. The Austrian theory of the business cycle explains every phenomenon exhibited by every business cycle, and further explains its historical onset (concomitant with central banking and/or fiat currency).

Recessions, while they may be postponed, cannot be avoided. As the eminent Austrian economist Ludwig von Mises noted:

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.[3]

Bernanke chose the latter (and has timed his exit superbly to cover his culpability). So what should he (or any central banker) have done when overseeing a recession? Only one directive applies: do not interfere with the economy’s adjustment process (a.k.a. recession). Do not prevent the liquidation of assets (or companies) with bailouts. Do not stimulate consumption and discourage savings through deficits and other means. And above all, do not inflate the money supply again which will only bring another recession in the future (which is why business cycles are, indeed, cyclical).

In light of what should not be done in a recession, Bernanke’s actions are an abject failure. For he responded to the Great Recession by advocating (with his Treasury troupe in tow) and/or performing a troika of trouble: big bailouts, huge deficits, and massive monetary expansion. In this dire economic situation, he responded with a disastrous blend of monetary omnipotence and judgmental incompetence.

The Bernanke legacy will eventually be known for what he has caused: severe recessions, high inflation, and just possibly, a “final and total catastrophe of the currency system involved.” We will never forget you Ben, nor forgive you.

von Mises, Ludwig. Human Action: A Treatise on Economics (Irvington: Foundation for Economic Education, 1996).

Christopher P. Casey, CFA®, CPA is a Managing Director at WindRock Wealth Management (www.windrockwealth.com). Using Austrian economic theory, Mr. Casey advises wealthy individuals on their investment portfolios to maximize their returns and minimize risk in today’s world of significant government intervention. Mr. Casey can be reached at 312-650- 9602 or at chris.casey@windrockwealth.com.

When Euphoria Turns to Phoria

January 2021

Financial market tops always exhibit elevated valuations (check) typically combined with weak or deteriorating economic conditions (check) and a backdrop of investor complacency (check). But the greatest bubbles exhibit far more than such excess; they exude exuberance. Are the financial markets in a current state of euphoria with a commensurate risk of a market downturn? Various metrics strongly indicate as such.

Citi provides their own proprietary index: the Citi Panic / Euphoria Model. This index utilizes multiple sentiment and trading indications to assess investor mentality. “Euphoric” measures exceed 0.41 on their scale. The market rarely reaches such levels: over the last 20 years, it breached this level only five times. Three of those were but brief touches before receding in quick order.

But two times, the market was solidly deep within the “euphoric” area of the index: 1999 to 2000 and 2020 to 2021. At the height of the technology bubble, the index neared 1.50. What does the index indicate today? In January 2021, the index sits solidly at 1.80 having gone hyperbolic over the last several months.1

Another commonly accepted signal of extreme bullish sentiment is the increased acceptance of and demand for riskier assets; for example, initial public offerings (“IPOs”). During such times, companies oblige by increasing the number of IPOs to avail themselves of such demand in raising capital. The following chart demonstrates the number of IPOs in 2020 exceeded even that of the technology bubble.2

Curiously, of the 480 IPOs in 2020, fully 248 of them were Special Purpose Acquisition Companies (SPACs).3 A SPAC is often called a “blank check” shell corporation because it pools investor funds together to finance an unknown acquisition within a future timeframe (generally two years).4 Investing in a SPAC is like paying to sit at the chef’s table in an unknown restaurant with an unnamed chef at some point in the future. Even the most fervent foodies would choke on the idea.

But not investors – not only were 248 SPACs debuted in 2020, but already to date in 2021, another 59 launched which tied the previous, pre- 2020 high set in 2019. And prior to 2019, SPACs averaged less than 17 per year during the previous ten-year period (2009 to 2018).5 If the Citi Panic / Euphoria Model seeks corroboration, IPOs and SPACs provide it.

While “euphoria” is a state of intense excitement and happiness, “phoria” is a misalignment of the eyes which breaks binocular vision. Investors are moving from euphoria to phoria: unable to focus on sound investment principles and blind to economic dangers.

As long the Federal Reserve continues aggressive monetary expansion, investors may continue to fuel financial markets to loftier valuations and higher euphoria. However, many variables could work to undermine or overwhelm the Federal Reserve’s efforts. If that happens, investor sentiment and demand may plummet, for their feelings are usually fickle. Financial markets will move accordingly.

Endnotes:

“A $13 Trillion Crisis-Era Debt Bill Comes Due for Big Economies” Bloomberg News. 04 January 2021

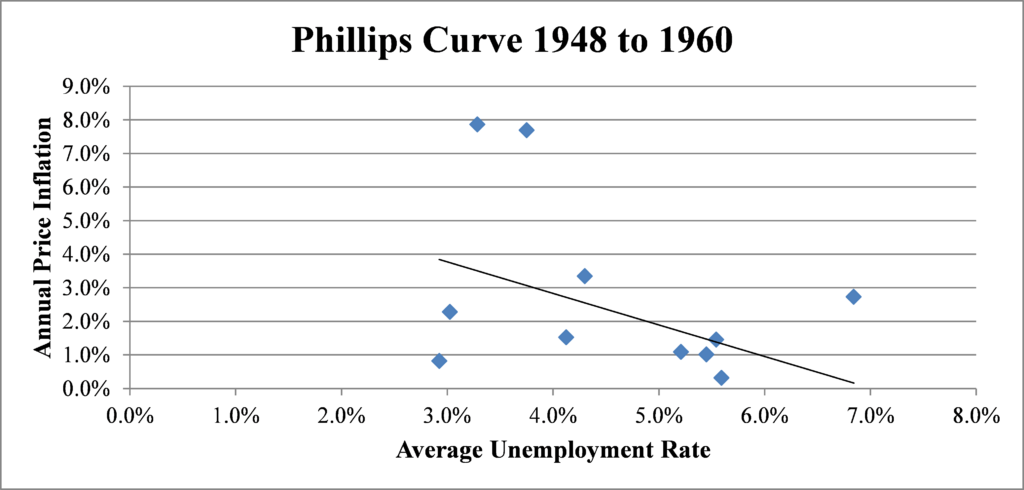

Anyone reading the regular Federal Open Market Committee press releases can easily envision Chairman Yellen and the Federal Reserve team at the economic controls, carefully adjusting the economy’s price level and employment numbers. The dashboard of macroeconomic data is vigilantly monitored while the monetary switches, accelerators, and other devices are constantly tweaked, all in order to “foster maximum employment and price stability.”1The Federal Reserve believes increasing the money supply spurs economic growth, and that such growth, if too strong, will in turn cause price inflation. But if the monetary expansion slows, economic growth may stall and unemployment will rise. So the dilemma can only be solved with a constant iterative process: monetary growth is continuously adjusted until a delicate balance exists between price inflation and unemployment. This faulty reasoning finds its empirical justification in the Phillips curve. Like many Keynesian artifacts, its legacy governs policy long after it has been rendered defunct.

In 1958, New Zealand economist William Phillips wrote The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957.2 The paper described an apparent inverse relationship between unemployment and increases in wage levels. The thesis was expanded in 1960 by Paul Samuelson in substituting wage levels with price levels. The level of price inflation and unemployment were thereafter linked as opposing forces: increasing one decreases the other, and vice versa. The US data from 1948 through 1960 comparing the year-over-year increases in the average price level with the average annual unemployment rate seemed irrefutable:3

The first dent in the Phillips curve came from Chicago-School economist Milton Friedman (as well as, independently, Edmund Phelps) who suggested it was more temporary than timeless, more illusion than illustration. Friedman’s “fooling model” posited that price inflation fooled workers into accepting employment at “higher” wage rates despite lower real rates as measured after the impact of price inflation. Once they realized the difference between “real” and “nominal” wages (the fools!), they would demand higher nominal rates as compensation. As inflation rose, unemployment declined, but only temporarily until a new equilibrium was achieved. This simple insight created quite a stir and troubled noted econo-sadist Paul Krugman: “when I was in grad school, I remember lunchtime conversations that went something like this; ‘I just don’t buy the … stuff — it’s not remotely realistic.’ ‘But these people have been right so far, how can you be sure they aren’t right now?’”4

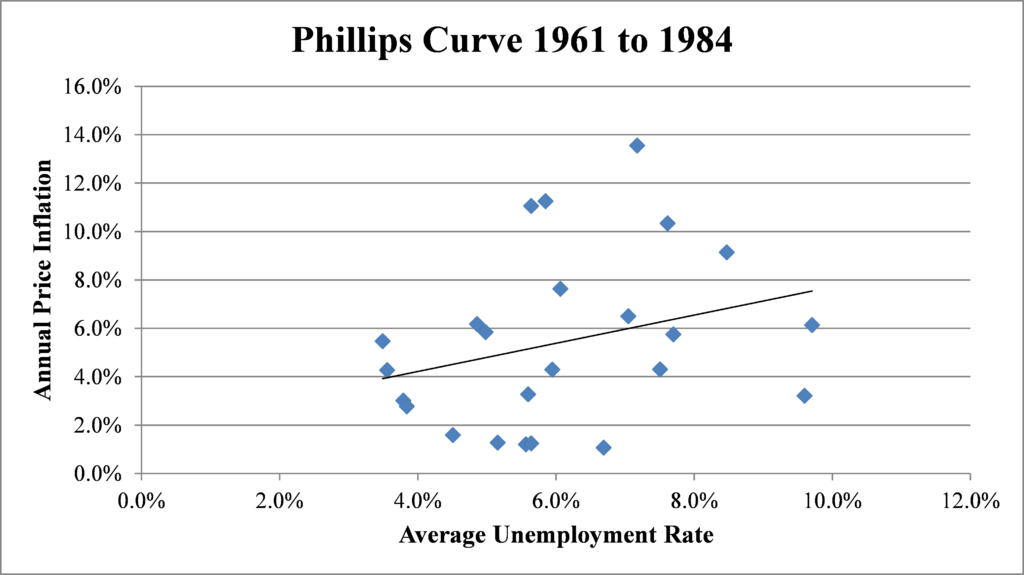

The Friedman criticism was somewhat clever, but unnecessary, minor, and misguided, for cold data was far more damaging than Chicago doctrine. The Phillips curve not only evaporated with the 1970s, but reversed to show a positive correlation between price inflation and unemployment:

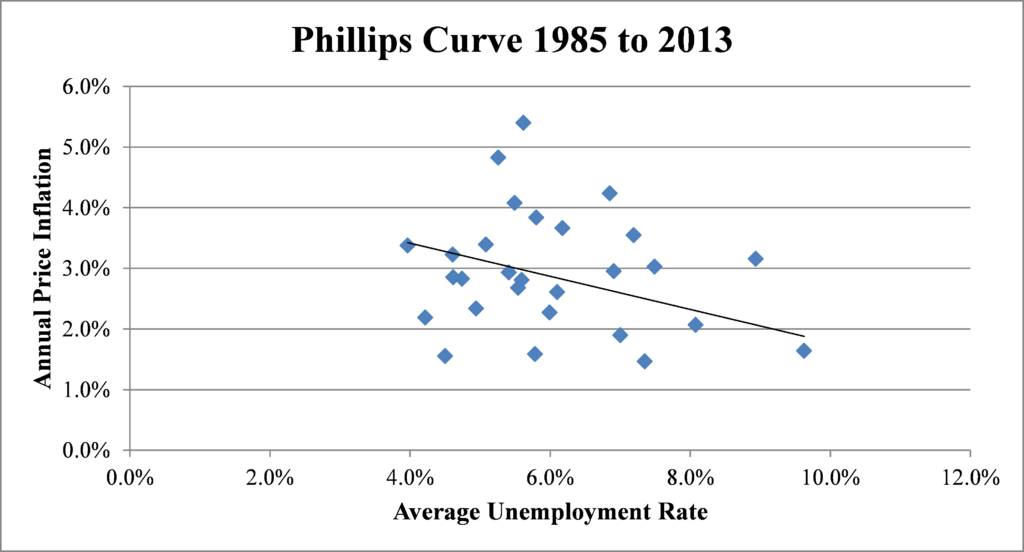

In light of this, like many Keynesian concepts, the Phillips curve should have been forever abandoned when the 1970s proved high price inflation and unemployment rates can coexist. But now the Phillips curve is back from the dead. Krugman, writing in 2013, introduced new data demonstrating the Phillips curve’s “resurrection.” According to Krugman: How many economists realize that the data since around 1985 — that is, since the Reagan- Volcker disinflation — actually look a lot like an old-fashioned Phillips curve?

This Krugman comment is correct, US data from 1985 through 2013 again shows an inverse correlation between the year-over-year increases in the average price level with the average annual unemployment rate:

Has the Phillips curve, as Krugman suggests, regained its former acceptance? Since 1985, why has its inverse relationship between price inflation and unemployment reappeared? The question is irrelevant: the fact that it had previously disappeared forever strips the Phillips curve of legitimacy.

Any apparent correlation between two variables may be coincidental and unrelated, directly casual, or linked by a third variable or sets of variables. For price inflation and unemployment, the last explanation is the correct one. Price inflation and unemployment are not opposing forces, but in large part effects deriving from the same causation — the expansion of the money supply.

More money cheapens its value and the price of goods and services accordingly rise in terms of money — hence price inflation. More money lowers interest rates which induce malinvestments (including the hiring of workers) which (who) are eventually liquidated (terminated) in a recession — hence unemployment. While both phenomena largely share a common origin, the timing of their manifestations may be quite different and heavily dependent upon other variables, including fiscal policy.

The death of the Phillips curve will eventually be served not from Chicago School gimmicks, not from the experience of the 1970s, but from greater acceptance of the Austrian School’s explanations of price inflation and business cycles. Unfortunately, in the interim, the monetary policies promoted by the Phillips curve have moved from 1970s lunchtime academic discussion to official government policy. In the hands of the Federal Reserve, the Phillips curve becomes weaponized Keynesianism.

Due to its unjustified acceptance of the Phillips curve and its related misconceptions about price inflation and business cycles, the Federal Reserve will never be able to trade higher price inflation for lower unemployment. Nor can it sacrifice higher unemployment for lower price inflation. But it can, and likely will, generate high levels of both. If the Federal Reserve’s economic controls appear broken, it is because they never really worked in the first place.

Endnotes:

Press release [2]. Federal Open Market Committee. Board of Governors of the Federal Reserve System. 30 April 2014.

William Phillips, “The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957,” Economica 25, No. 100 (1958): 283–299.

Federal Reserve Bank of St. Louis. In the interest of aesthetics and clarity, years for which a negative price inflation or unemployment rate have been excluded. However, their visual exclusion does not alter the linear trendline presented in the following graphs.

Higher equity prices will boost consumer wealth and help increase confidence, which can spur spending. — Ben Bernanke, 2010.1

Across all financial media, between both political parties, and among most mainstream economists, the “wealth effect” is noted, promoted, and touted. The refrain is constant and the message seemingly simple: by increasing people wealth through rising stock and housing prices, the populace will increase their consumer spending which will spur economic growth. Its acceptance is as widespread as its justification is important, for it provides the rationale for the Federal Reserve’s unprecedented monetary expansion since 2008. While critics may dispute the wealth effect’s magnitude, few have challenged its conceptual soundness.2 Such is the purpose of this article. The wealth effect is but a mantra without merit.

The overarching pervasiveness of wealth effect acceptance is not wholly surprising, for it is a perfect blend of the Monetarist and Keynesian Schools.3While its exact parentage and origin appears uncertain, its godfather is surely Milton Friedman who published his permanent income theory of consumption in 1957.4In bifurcating disposable income into “transitory” and “permanent” income, Friedman argued the latter dictates our spending and consists of our expected income in perpetuity. If consumer spending is generated by expected income, then surely it must also be supported by current wealth?

But this may or may not be true. It will vary across time, place, and among various economic actors whose decisions about consumer spending are dictated by their time preferences. And time preferences — the degree to which an individual favors a good or service today (consumption) relative to future enjoyment — take into account far more variables than the current, unrealized wealth reported in brokerage statements and housing appraisals.

Regardless as to whether or not increased wealth will actually spur increased consumer spending, the most important component of the wealth effect is the assumption that increased consumer spending stimulates economic growth.5 It is this Keynesian concept which is critical to the wealth effect’s validity. If increased consumer spending fails to stimulate the economy, the theory of the wealth effect fails. Wealth effect turns into wealth defect.

Will increased consumer spending improve the economy? On one side of the argument, we have the aggregate individual conclusions of hundreds of millions of economic actors, each acting in their own best interest. These individuals and businesses are attempting to reduce consumer spending and increase savings.

Dissenting from their views are the seven members of the Board of Governors of the Federal Reserve. Each member believes in the paradox of thrift — the belief that increased savings, while beneficial for any particular economic actor, have deleterious effects for the economy as a whole. The paradox of thrift can essentially be described as such: decreased consumer spending lowers aggregate demand which reduces employment levels which negatively affects consumption which in turn lowers aggregate demand. The paradox predicts an economic death spiral from diminished demand. And mainstream economists believe we were (and potentially are) mired in such a spiral. As noted econo-sadist Paul Krugman noted in 2009: “we won’t always face the paradox of thrift. But right now it’s very, very real.”6

The inverse of this “reality” predicts flourishing economic prosperity when a society increases its consumer spending. But history suggests the opposite: it is higher savings rates which lead to economic prosperity. Examine any economic success story such as modern China, nineteenth century America, or post-World War II Japan and South Korea: did their economic rise derive from unbridled consumption, or strict frugality? The answer is self-evident: it is the savings from the curtailment of consumption, combined with minimal government involvement in economic affairs, which generates economic growth.

So why do so many “preeminent” economists falsely believe in the paradox of thrift, and thus the wealth effect? It is because of their mistaken understanding of the nature of savings. The Austrian economist Mark Skousen addressed this in writing:

Savings do not disappear from the economy; they are merely channeled into a different avenue. Savings are spent on investment capital now and then spent on consumer goods later.7

Savings are spent. Not directly by consumers on electronics and espressos, but indirectly by businesses via banks on more efficient machinery and capital expansions. Increased savings may (initially) negatively affect retail shops, but it benefits producers who create the goods demanded from the increased pool of savings. On the whole, the economy is more efficient and prosperous.

Does this economic maxim hold even when the economy is in a recession?8Even more so. As all Austrian economists know, business cycles derive from government manipulation of the money supply which artificially lowers and distorts the structure of interest rates.9To minimize the length and severity of a recession, economic actors should save more which will reduce the gap between artificial and natural rates of interest.

Regrettably, this is not merely an academic discussion. Due to their mistaken economic beliefs, the Federal Reserve has quadrupled the money supply while bringing interest rates to historic lows.10The results will inevitably arise: significant price inflation, volatile financial markets, and severe economic downturns. In many respects, Sir Francis Bacon’s aphorism that “knowledge is power” is true. Unfortunately, in the economic realm, the Austrian economist F.A. Hayek was closer to the truth: those in power possess the pretense of knowledge.11

To date, most criticism focuses on the relatively minor increase in real GDP (11.2 percent from April 1, 2009 through October 1, 2013) relative to the substantial increases in the money supply and the stock market which have risen, respectively, 330.0 percent (Adjusted Monetary Base from August 1, 2008 through January 1, 2013) and 160.9 percent (S&P 500 from March 1, 2008 through February 19, 2014). The dates have been selected to measure the increase since the respective lows reached subsequent to August 1, 2008 to the most recent data.

The characterization of monetarism as an economic school can be disputed. By definition, a school of thought must be systemic, which means positions and theorems must be connected by underlying assumptions. The so-called Monetarist School consists of various unrelated hypotheses which are empirically “tested.” While the preponderance of the “school’s” positions may favor free markets (although often not for the most critical markets — e.g., money), they display inconsistency in application. This underscores the lack of an academic edifice built from fundamental axioms.

Milton Friedman, Theory of the Consumption Function. Princeton, N.J.: Princeton University Press; Homewood, Ill.: Business One Irwin. 1957.

The commonly cited support for this assertion, that personal consumption accounts for approximately 70 percent of Gross Domestic Product is, strictly speaking, correct. However, it is correct only because GDP overstates personal consumption as a by-product of a misguided attempt to avoid “double counting.” If non-durable capital goods and intermediate products (e.g., steel) were included in GDP (as they should be if one is attempting to measure economic activity), personal consumption would fall to approximately 40 percent of economic activity based upon the latest GDP component and Gross Output statistics. Mark Skousen, “Beyond GDP: Get Ready For A New Way To Measure The Economy.” Forbes. 29 November 2013.

Mark Skousen, Economics on Trial. Homewood, Ill.: Business One Irwin, 1991. p. 54.

It would be odd indeed if one argued that savings increases economic growth during normal times, but exiting a recession requires greater levels of consumption. As Ayn Rand wrote: “Contradictions do not exist. Whenever you think you are facing a contradiction, check your premises. You will find that one of them is wrong.” (Atlas Shrugged, New York: Random House, 1957). If economic growth during a recession requires increased consumption, then this business cycle theory does not comport with general economic theory — which is prima facie evidence that it is wrong.

It should be noted that an increase in consumer spending due to increased levels of real or perceived wealth in no way invalidates or contradicts Austrian business cycle theory (“ABCT”). While some economists have alleged increased consumption during the boom phase of a business cycle is in conflict with ABCT, Austrian economist Joseph Salerno has effectively squashed such criticisms as a misinterpretation. (Joseph Salerno, “A Reformulation of Austrian Business Cycle Theory in Light of the Financial Crisis,” Quarterly Journal of Austrian Economics. 15, No.1. [2012]).

See footnote 2.

“To act on the belief that we possess the knowledge and the power which enable us to shape the processes of society entirely to our liking, knowledge which in fact we do not possess, is likely to make us do much harm.” F.A. Hayek, “The Pretense of Knowledge.” Lecture to the Memory of Alfred Nobel. Stockholm Concert Hall. Stockholm, Sweden. 11 December 1974.

And the Election Winner is … Inflation in a Landslide!

Christopher P. Casey

Regardless as to which candidate secures the Presidency on November 3rd (or some subsequent date), the administration must cope with unprecedented federal debt. This debt will only increase for the foreseeable future with record-breaking federal deficits caused by mounting pandemic relief and stimulus spending along with diminished tax revenues. The only available “solution” for the U.S. government to finance such debt and deficits will be through continued massive money printing which will inevitably lead to price inflation. How can investors protect themselves?

What Does and Does Not Cause Inflation?

Due to the widespread misunderstanding of what causes inflation, it first warrants a discussion as to what does not cause inflation. In particular, three inflation fallacies are often cited by mainstream financial pundits and Keynesian economists.

First, the “cost-push” theory of inflation states that price increases in certain commodities force the prices of all goods and services higher. The 1970s are often cited as an example: as increased oil prices permeated the economy, prices for fuel, plastics, and other oil-derived products would increase as well.

But as the price of oil or some other cost-push culprit rises, buyers have less money to spend on other goods and services. Having less money to purchase something else means less demand exists for that other product, and decreased demand reduces prices. So, while some prices may go up, it is ultimately at the expense of other prices which go down. Accordingly, no direct net effect to the overall price level is created by these price changes.

The second inflation misconception is the “demand-pull” theory. Keynesian economic theory believes inflation also materializes when aggregate demand for goods and services exceeds aggregate supply when the economy is at full employment and capacity (which also incorrectly assumes such “aggregates” can diverge from each other). When the economy is at full employment and capacity, increased aggregate demand forces producers of goods and services (soon to be followed by their suppliers) to increase prices. Here lies the origin of the belief in inflation from an “overheated” economy. According to this theory, inflation cannot develop during periods of weak economic growth. But the 1970’s American economy (as well as numerous other economic periods in history – see modern-day Venezuela) clearly disprove this.

Finally, many incorrectly believe inflation cannot develop until the “velocity” of money increases. Typically defined as “the number of times one dollar is spent to buy goods and services per unit of time,” monetary velocity theory originates from the so-called Fisher Equation of Exchange: MV=PT (where the quantity of money [M] times the velocity of its circulation [V] equals prices [P] multiplied by their related transactions [T]). But why would such a formula explain the general price level?

Almost all economists today recognize that the price for any particular good or service derives from the interaction of supply and demand. The “price” of money derives from the same supply and demand dynamic as any good or service. The word “price” in terms of money, to avoid confusion, can be thought of as “value”. If the demand for money increases, its value increases and the prices of all goods and services fall (deflation). If the supply of money increases, its value decreases and the prices of all goods and services rise (inflation). Inflation is simply caused by an increase in the money supply and/or a reduction in the demand for money.

Velocity is not a substitute for demand, but rather of volume. Lots of goods and services may transact at low prices just as they may trade at high prices. In either scenario, “velocity” is high while the demand for money may be low or high. Since velocity is not a substitute for demand, it cannot help explain inflation.

How Does the Federal Debt Situation Affect Inflation?

Federal debt can be deleterious for many reasons. Among other things, it crowds out private investment (by bidding up the price of capital) and must be repaid by taxpayers (in one form or another). The repayment must derive from future taxes or by printing new money to satisfy debt service.

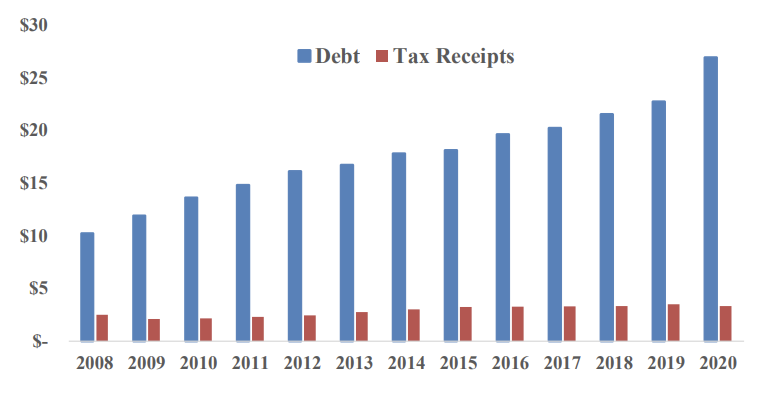

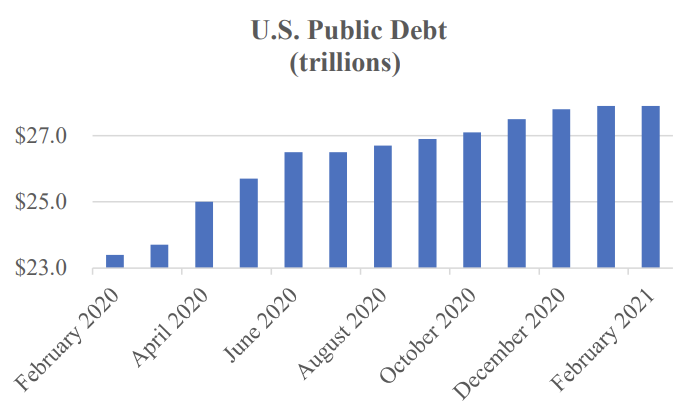

As this chart demonstrates, the U.S. government can never repay its debt based upon tax receipts (nor do politicians have any intention of doing so) (in trillions):1

As of September 30, 2020, the federal debt stood at over eight times estimated 2020 fiscal year tax receipts.2

It would take that many years to repay all debt assuming the federal government ceased all spending. Paying back the federal debt through future budget surpluses is unrealistic. And the situation is getting worse.

The Congressional Budget Office, itself always opportunistic about government finances, recently stated “the deficit in 2021 is projected to be 8.6 percent of GDP.” And that “between 1946 and 2019, the deficit as a share of GDP has been larger than that only twice”.3

The only means by which the U.S. government can service its debt, let alone its future debt, is through continued, massive monetary expansion. And the Federal Reserve has already started in record-breaking fashion:4

Why Should Investors be Concerned?

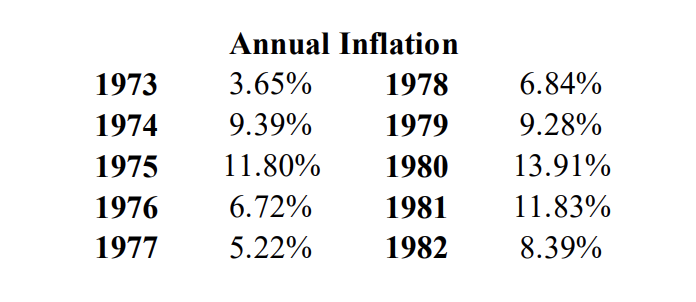

Many U.S. investors have little memory of the 1970’s inflation and thus not only discount the likelihood of inflation, but are largely ignorant as to its negative impact. It bears remembering that the price level did in fact more than double (121% increase) in approximately ten years (from 1973 to 1982).5

The implications for traditional stock and bond portfolios can be devastating. For example, in real terms, a 60%/40% stock/bond portfolio from 1973 to 1982 returned an annual rate of less than 1% (when calculated using the Wilshire 5000 Total Market Index as a proxy for equities and the ICE Bank of America U.S. Corporate Index Total Return Index Value to represent bonds).6

Bonds were especially impacted, losing just over 4% per annum which disproportionately affected retirees, those approaching retirement, and any “conservative” investors.

The 1970s demonstrate that, at least in regards to inflation, stocks and bonds may not provide significant diversification to each other.

What can Investors do to Protect Themselves from Inflation?

Inflation-protection hedges fall into three categories. First, and perhaps most obvious, alternative currencies which are not experiencing the same inflationary pressures. For many years, foreign currencies such as the Swiss franc qualified (until the Swiss National Bank embarked on the same reckless monetary expansion as the world’s other major central banks). But precious metals and cryptocurrencies provide even better protection.

Second, any businesses which have costs in an inflationary currency with revenues tied to a stable (or at least less inflationary) currency profit from the currency valuation discrepancies, and should appreciate dramatically. Primarily, this involves commodity producers such as farmland or energy companies. Some potential examples would be American farmland in the 1970s (and in the future), Brazilian farmland today, or Russian energy companies during any ruble crisis.

Finally, assets utilizing extensive financial leverage (especially with long-term fixed rates) should also perform well. Since inflation helps borrowers to the detriment of lenders (since the money repaid is worth less than when lent), industries with large debt levels such as real estate benefit (especially if they have short- term leases with tenants that renew at the new, inflationary rents). Additionally, as inflation may increase interest rates which deters or limits future borrowing, such industries may experience less future competition, all things being equal.

But the marketplace already knows about these traditional inflation hedge categories. The time to act is before the prices of inflation-protection assets are bid up once inflation appears.

About WindRock

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high-net-worth individuals, family offices, foundations and retirement plans.

“An Update to the Budget Outlook: 2020 to 2030” Congress of the United States Congressional Budget Office. September 2020

Federal Reserve Board of St. Louis https://fred.stlouisfed.org/

Ibid.

Ibid.

Problems with Today’s Wealth Management Industry

Christopher P. Casey

Question: Although WindRock Wealth Management is a U.S.-based Registered Investment Advisor which manages money for wealthy individuals, you certainly seem different from other firms out there. One of those differences is your macroeconomic viewpoints. Why is that important to WindRock?

WindRock: It is amazing but true, many wealth advisory firms have no view on the economy! I cannot tell you how many times I have asked Chief Investment Officers of major wealth advisory firms what causes recessions, and their response is either “we don’t know” or “we’re agnostic as to the economy” – whatever that means. If any firms hold any views on the economy, they typically adhere to Keynesian economics – they basically just parrot what the Federal Reserve and other mainstream organizations predict. And the Federal Reserve in particular has a horrific track record in this regard – having not only completely missed the 2008 recession and the 2007 housing crisis, but also by initially dismissing the impact of Covid on the economy.

So, we think having a well-thought-out view on the economy is a tremendous advantage. We think it’s important in designing portfolios. In particular, we favor the Austrian school of economics which is an alternative to Keynesian philosophy. Austrian economists, unlike the mainstream Keynesian economists, understand what truly causes inflation and recessions – the artificial expansion of the money supply by central banks. Since these are the two greatest threats to anyone’s investment portfolio, this understanding is critical. This is why many wealth advisory firms herded their clients right over the cliff with the crash in technology stocks and later with all equities in 2008 – which we can see repeating in the future. They could not foresee these events because those events don’t comport to their flawed models and theories. For the same reason, they do not foresee any danger with today’s overvalued U.S. stock and bond markets. By using Austrian economics, we have a time-tested tool to guide our decisions.

Question: Recessions pop asset valuations, and are thus a threat to anyone’s portfolio, but what about inflation? What do you see going forward and how do you position clients accordingly?

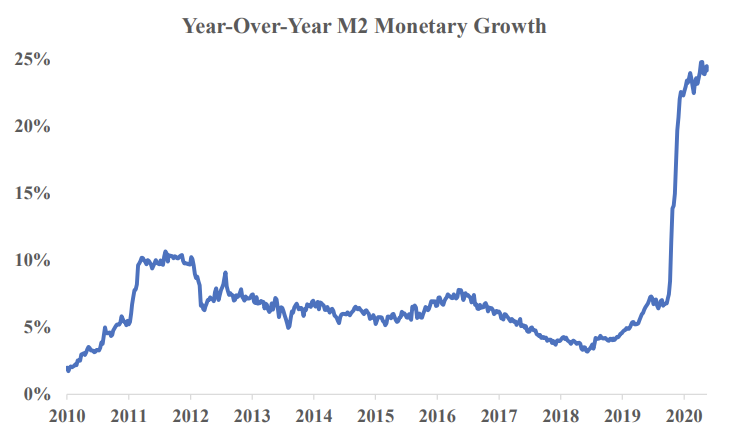

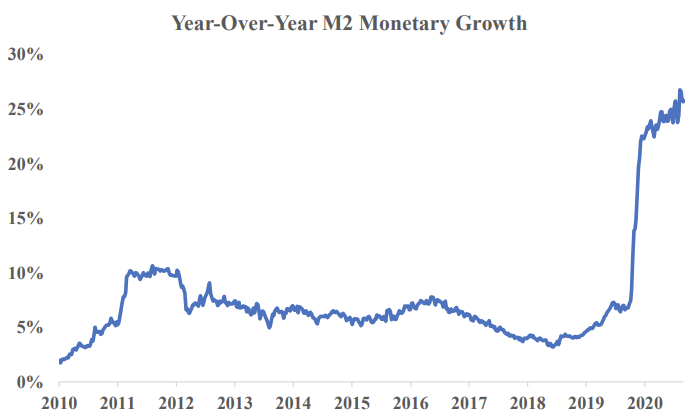

WindRock: The actions of the Federal Reserve since August 2008 – and especially since March 2020 – are truly unprecedented. Depending on how you measure it, the U.S. money supply has increased over 75% since the lockdowns were initiated. We’re at historically high year-over-year growth rates – and we have been since March 2020. Increasing the money supply to this degree will inevitably cause significant inflation. It may not show up soon, it may even be preceded by some brief deflation – although I doubt that, but it will develop. When this happens, stocks will, at best, be flat in real terms. And bonds will be decimated. The only way to protect one’s wealth is to invest in such thing as precious metals, cryptocurrencies like bitcoin, and certain types of real estate – mainly farmland and rental residential real estate in the Sun Belt states. Positioning one’s portfolio as such will not only offer protection, but great profit. And this isn’t just based in theory, but in experience. The historical performance of these investments in the 1970’s in America offers great guidance – while the price index more than doubled in 10 years, farmland and gold provided tremendous appreciation.

Question: How do you design portfolios?

WindRock: Our clients’ risk profiles and liquidity needs are integrated with our projections of real economic growth and price levels over the next twelve months. We then combine this with our judgment as to overall asset valuations in the equity and debt markets to determine the allocation between stocks, bonds, and hard assets such as real estate and precious metals. After determining these broad allocations, those same assessments dictate the constituent parts of each allocation. For example, if we are in equities, how much is in emerging markets versus the developed world? How much is defensive versus aggressive, etc.?

One additional item I should note about portfolio construction, we do not believe in “putting all of your chips on red” and waiting for the big payoff. By that I mean we select investments we expect to do very well when the economy plays out the way we expect, but they will also do well in the interim due to the compelling risk and return profile the investment itself offers. As an example, we believe multi-family rental real estate will do quite well in the U.S. when a housing decline unfolds due to rising interest rates and/or inflation hits. Our play has been to focus on new construction neighborhoods that rent like apartments but look and feel like single family homes. We did not go out and buy a publicly traded rental real estate vehicle – they are currently overvalued – which may do well in a housing decline and/or with inflation – we found an investment which believe will do well regardless since it is building a new type of multi-family housing community.

Question: What else differentiates WindRock from other wealth advisory firms?

WindRock: It’s not just about having a different view on how economies work. It’s about what you do with that knowledge. It’s about having an entrepreneurial mindset to act on these opportunities – to seek out and vet investment vehicles which the mainstream wealth advisory industry won’t touch. I think we describe this well on our website where we wrote:

Conventional wisdom associates the word “entrepreneur” with the assumption of risk. While risk can never be fully avoided, what actually makes entrepreneurs unique is their understanding of risk. Our unique insight of the risks posed by governmental interference in the economy serves to protect our clients’ wealth. As entrepreneurial-minded advisors, we emphasize independent and creative thought to boldly seize opportunities while minimizing key risks.

Farmland is a great example. There are very few public farmland vehicles – Real Estate Investment Trusts – or REITs, in the U.S. Accordingly, there are no investment benchmarks for farmland to be considered by mainstream wealth advisors (because the sample size is too small). Therefore, mainstream wealth advisory firms will not consider an investment in farmland. Mind you, it’s not because the investment opportunity isn’t there, but because they cannot be viewed as performing out of sync with the commonly used real estate investment benchmarks. To do otherwise will entail risking their careers. This is a real problem in the wealth advisory industry – advisors are worried about losing clients, not with losing clients’ money. The mainstream wealth advisors are happy tracking what everyone else is doing – because in so doing, they believe they are preventing their clients from switching to another firm. This “career risk” syndrome forces wealth advisors into short-term outlooks with a herd-like mentality.

This is a real problem in the wealth advisory industry – advisors are worried about losing clients, not with losing clients’ money.

Question: Besides the lack of an economic viewpoint (or an incorrect one), besides the “career risk” mentality, what other problems exist within the wealth advisory industry?

WindRock: Misaligned incentives. Many firms lack independence, meaning they create and market their own investment vehicles. So oftentimes they’re not just advising clients to own a particular type of investment – they’re advising clients to own their investment. Which certainly means additional fees and probably a sub- performing investment vehicle. I cannot tell you how many times I have reviewed a prospective client’s investments only to find they are heavily invested in their advisor’s funds. Is it really that likely that the best emerging market equity fund just happens to be owned and run by the advisor’s firm? That the very same advisory firm has the top currency fund? What are the odds?

Question: So, the XYZ Wealth Management firm owns the XYZ funds . . .

WindRock: I think common sense and anecdotal evidence suggests that if you examined client statements from all wealth advisory firms, you will not find the ownership dispersion you would expect if wealth advisors truly provided independent advice. This Wall Street sales culture permeates many firms. Unfortunately, the more wealth advisors serve as salesmen, the less they act as a trusted advisor.

Question: With all of these problems in the industry, why should investors even consider using a wealth advisor?

Unfortunately, the morewealth advisors serve as salesmen, the less they act as a trusted advisor.

WindRock: Doing it yourself can be an option. And perhaps a fairly viable one when compared to the alternative of using many of these firms. But there are still compelling reasons to use a wealth advisory firm. For example, since wealth advisors possess buying power by representing numerous clients, we can have access to certain investment vehicles which may simply be unavailable to the individual investor. In addition, we can negotiate lower fees and minimum investments with the funds we utilize. But in a greater context, maximizing returns and minimizing risks for any investment portfolio requires time, research, money, judgement, and knowledge. It’s a full-time job, especially in today’s world of massive government intervention in the economy and the financial markets, to manage a portfolio. This is why we created WindRock, because wealth advisory has its place – it just needs a different economic viewpoint, a unique investing mindset, and greater independence.

Question: How can anyone interested contact you to learn more about WindRock’s services?

WindRock: Of far greater importance than what we do is what we believe. All of our marketing is driven by thought-leadership, so I encourage any interested parties to visit our webpage at www.windrockwealth.com to read about our philosophy as well as our regularly posted research and analysis. I also suggest interested parties to sign up for our mailing list.

About WindRock

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high-net-worth individuals, family offices, foundations and retirement plans.

This article was originally published by the Mises Institute on August 29, 2018

Fans of HBO’s hit series, Game of Thrones, know well the motto of House Stark: “Winter is Coming.” This motto warns of impending doom, whether brought on by the Starks themselves, devastating multi-year, cold weather, or something far more ominous north of the Wall.

At least since Soviet economist Nikolai Kondratieff wrote The Major Economic Cycles in 1925, recessions have been associated with winter weather.1 Although Kondratieff’s theories contained as much fantasy as Game of Thrones, using seasons as an analogy for the stages of a business cycle is intuitive. If spring represents recovery, and summer the peak of economic growth, then the U.S. economy may well be in autumn. All should be as wary as the subjects of Westeros (the realm of focus in Game of Thrones).

Why Winter is Coming

Few mainstream economists currently foresee a recession. They cite “strong” (a new-found, favorite term in Federal Open Market Committee minutes) economic statistics, a “healthy” stock market (despite gains highly concentrated in the so-called “FANG” stocks), and few warning signs among the “leading indicators.”2 3 But the same exact sentiment existed before the last recession. Most infamously, then-Federal Reserve Chairman Ben Bernanke stated in January 2008 – exactly one month after the recession technically began: “the Federal Reserve is not currently forecasting a recession.”4

How could Chairman Bernanke have been so wrong then, and why may mainstream economists be likewise wrong today? The answer lies in their erroneous business cycle theories. Without a theory which accurately describes recessions, watching leading indicators or other signs of a slowdown are as effective as reading tea leaves. One can only predict by first understanding causality.

The Austrian school of economics explains business cycles, for it describes their phenomena (e.g., the “cluster of error” exhibited by businesses and economic actors), why they are recurring, and why they first repeatedly appeared in the 19th century (with fractional-reserve banking and/or central banks). In short, when the money supply is artificially increased, interest rates are decreased and distorted. As interest rates are a universal market signal to all businesses and economic actors, investments and purchases which previously appeared unprofitable or untenable now seem economically profitable or reasonable.

However, these expenditures are actually “malinvested” relative to the natural level of interest rates. When interest rates revert to their natural level and structure, a recession ensues. Recessions are an inevitable condition which corrects malinvestments by returning capital to rightful purpose.

What causes the artificial boom to end and the winter to begin? Ludwig von Mises offered a succinct explanation:

The boom can last only as long as the credit expansion progresses at an ever-accelerated pace. The boom comes to an end as soon as additional quantities of fiduciary media are no longer thrown upon the loan market.5

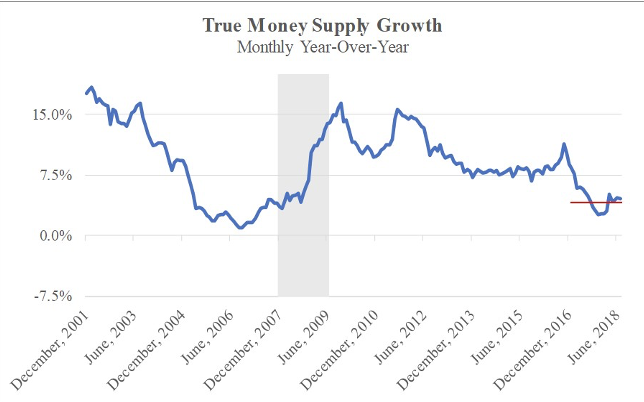

In the U.S., the growth rate of “additional quantities of fiduciary media” has flatlined (as represented by the red line below). The most relevant monetary metric to analyze is the Austrian definition of the money supply known as “True Money Supply” (“TMS”). Developed by Murray Rothbard and Joseph Salerno (and frequently commented upon by Ryan McMaken of the Mises Institute), TMS more accurately captures Federal Reserve activity than traditional measures such as M2. Since March 2017, it has averaged a mere expansion rate of just over 4%.6

Since Austrian business cycle theory describes the impact of monetary expansion and contraction upon interest rates which, in turn, impacts the economy, are interest rates likewise signaling a possible end to the current, artificial economic expansion?

When Winter is Coming

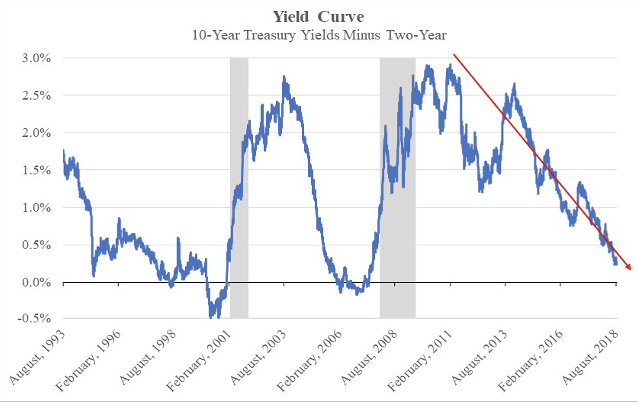

Interest rates have certainly risen. Since breaking below 1.4% just over two years ago, the 10-year Treasury has traded with a yield close to 3.0% for the majority of 2018.7 But in forecasting a recession, timing and probability are better served by analyzing the structure of interest rates (known as the yield currve) rather than the overall interest rate level.

The yield curve represents a graphical depiction of fixed-interest rate security yields plotted against the amount of time until their maturity. Various methods of measuring the “flatness” of the yield curve exist, but one of the most popular is the yield on a long-dated bond (e.g., the 10-year Treasury) minus the yield on a shorter-term bond (e.g., the 2-year Treasury). Based on this methodology, the yield curve has flattened extensively over the last several years to levels last observed just prior to the Great Recession.

Historically, a yield curve which flattens enough to become inverted; that is, when short-term interest rates are higher than longer-term interest rates, a recession typically follows. An inverted yield curve possesses a unique power of predictability.

As explained by economist Robert Murphy, in foreshadowing every recession since 1950:

Not only has there only been one false positive (which even here was still associated with a slowdown), but every actual recession in this timeframe has had an inverted (or nearly inverted) yield curve precede it. In other words, there are no false negatives either when it comes to the yield curve’s predictive powers in the postwar period.7

The acknowledgement of the yield curve’s prognosticative capability extends beyond Austrian school economists such as Dr. Murphy, for numerous studies – many by Federal Reserve economists – cite this phenomenon. The Federal Reserve Bank of New York, in introducing some of this research, recognizes “the empirical regularity that the slope of the yield curve is a reliable predictor of future real economic activity.”8

Recognition is different from understanding as mainstream economists are largely unable to offer an explanation. However, yield curve recession signals adhere well to Austrian business cycle theory which demonstrates the importance of banks in creating money and lowering interest rates (which steepens the yield curve as most of their influence resides with shorter maturities). It is the reversal of money creation – and the impact of banks on interest rates – which causes shorter-term interest rates to rise disproportionately (the typical fashion by which the yield curve flattens).

In addition, if the artificial boom ends when interest rates are no longer artificially depressed, then it stands to reason the structure of interest rates will also revert to its natural state. A flatter yield curve comports with the natural structure of interest rates expected in a free market. The Austrian-economist Jesús Huerta de Soto described the underlying reason free markets generate flatter yield curves:

. . . the market rate of interest tends to be the same throughout the entire time market or productive structure in society, not only intratemporally, i.e., in different areas of the market, but also intertemporally . . . the entrepreneurial force itself, drive by a desire for profit, will lead people to disinvest in stages in which the interest rate . . . is lower, relatively speaking, and to invest in stages in which the expected interest rate . . . is higher.9

In short, the predictive power of the yield curve is matched only by the explanatory power of Austrian business cycle theory. If it continues to flatten and invert, a recession will likely follow as the previously created malinvestments are exposed.

But rather than wholeheartedly embrace yield curve analysis, high-ranking Federal Reserve officials consistently waffle at its utilization. Like Westerosi maesters in conclave to determine the advent of winter, they frequently recognize recessions only after their onset.10

Conclusion

The similarities between the climate in Game of Thrones and the state of the U.S. economy are eerily similar. Prior to the recent beginning of winter, Westeros experienced an unusually long time since the last winter. Likewise, according to the National Bureau of Economic Research, the current U.S. expansion is the second longest ever at just over nine years (110 months).11

Also, just as recessions are not phenomena endogenous to free markets (but rather, as discussed above, caused by an artificial expansion of the money supply typically produced/coordinated by central banks), so too the winters in Westeros appear to be generated from an artificial, exogeneous source. As protagonist John Snow explained in describing the supernatural White Walkers: “the true enemy won’t wait out the storm. He brings the storm.” The Night King is the Westerosi version of the Chairman of the Federal Reserve (with the primary difference being the Night King purposely brings about winter).

Finally, like the next winter in Westeros, the next U.S. recession may prove unusually severe by historical standards. In Game of Thrones, many characters (at least the peasants) believe this winter will be the worst in 1,000 years. Given the Federal Reserve’s unprecedented monetary machinations since 2008, the next recession may well prove worse than the last one, and potentially as devastating as the Long Night.

Approximately one year ago, speaking as confidently as a Red Priestess of R’hllor, then-Federal Reserve Chair Janet Yellen believed the next recession-driven financial crisis may be averted for at least a generation or so:

Would I say there will never, ever be another financial crisis? . . . Probably that would be going too far. But I do think we’re much safer . . . and I hope that it will not be in our lifetimes, and I don’t believe it will be [emphasis added].12

You know nothing, Janet Yellen. Winter is coming.

About the Author: Christopher P. Casey is a Managing Director with WindRock Wealth Management. Mr. Casey advises clients on their investment portfolios in today’s world of significant economic and financial intervention. He can be reached at 312-650- 9602 or chris.casey@windrockwealth.com.

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high net worth individuals, family offices, foundations and retirement plans.

All content and matters discussed are for information purposes only. Opinions expressed are solely those of WindRock Wealth Management LLC and our staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Fee-based investment advisory services are offered by WindRock Wealth Management LLC, an SEC-Registered Investment Advisor. The presence of the information contained herein shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services except, where applicable, in states where we are registered or where an exemption or exclusion from such registration exists. WindRock Wealth Management may have a material interest in some or all of the investment topics discussed. Nothing should be interpreted to state or imply that past results are an indication of future performance. There are no warranties, expresses or implied, as to accuracy, completeness or results obtained from any information contained herein. You may not modify this content for any other purposes without express written consent.

WindRock Roundtable: What Does the Rest of 2021 Hold for Investors?

Most financial publications have an annual roundtable of Wall Street economists or mainstream financial commentators, all of whom share very similar viewpoints.

WindRock’s annual roundtable features independent investment minds.

WindRock: Let’s start with the 2021 impact of three major 2020 developments: the election, social unrest, and the Covid-imposed lockdowns. First, we have a new Biden administration with a Democratically controlled Congress. What do you think will be the most likely major legislation to pass? Will that include rolling back anything Trump did?

Mauldin: In one sense, it’s not an ideal world if you’re a Democrat. You get blamed for everything, but you don’t have a whole lot of control. Even though they technically have control of Congress, if they lose a couple of moderates, you’ve lost your majority (with the tie cast by the vice president) in the Senate. So, I don’t think they’re going to be able to go too far with their agenda. [Speaker of the House] Pelosi has the same problem. She gets five or six of her members to switch party lines on votes, and she’s lost her majority. It’s a razor-thin margin.

So, I don’t expect radical legislation. I would expect to see an infrastructure bill for which, frankly, if we’re going to run up the national debt on stimulus acts, I would rather run it up with actual, honest-to-God infrastructure. I’m talking roads, bridges – the stuff that we need to get repaired.

I would like to see the creation of something like a Ginnie Mae for infrastructure so that cities can borrow money to fix their own infrastructure. There’s a lot of cities that need to rebuild their water systems. They can tack on a penny a gallon or whatever the number would work to retire that debt if you can borrow at 1- 2%. The Fed [Federal Reserve] can buy those bonds legitimately because it’s a government-backed asset. You’d have to put restrictions around it; it’d have to be something that would be self-liquidating as opposed to general obligation bonds. You could really do a whole lot of good. I mean, just spending $30-$40 billion on updating the utility grid will save us more than that on our power bills over a few years.

As much as I’m critical of lots of things that China has done, they’ve built an enormous amount of infrastructure, and it clearly shows in their growth rates. We can do that here. For example, we just finished dredging the Mississippi at its mouth so we can now get Panamax container ships up to Memphis. That’s going to be huge. Now they don’t have to stop at the Port of Los Angeles or anywhere else on the west coast. I mean, they can come right into the middle of America and get right off onto trains. That’s going to cut out an enormous amount of costs.

Dirlam: Our feeling – even prior to the Georgia runoffs – was that whatever the political composition of government, there was going to be a lot of spending. The budget deficit was just going to go through the roof. Part of that was seeing how 2020 played out and gauging how markets would tolerate so much deficit spending and with so much monetization of debt by the Fed. In the fourth quarter [2020], the Fed basically bought a third of all Treasury issuance which was about $600 billion. So, we think with this so-called a “blue sweep”, there will be even more spending involved.

They will also likely roll back some of what Trump did. I go back and forth on what will happen with Trump’s tax cuts [the 2017 TCJA]. They certainly don’t have to increase taxes – simply because the markets are so willing to tolerate these levels of deficits and debt monetization. It would be a very politically powerful move to roll back tax cuts, so if one of the administration’s first moves is to do that, I think that’s a pretty strong political statement, especially because there wasn’t a voter mandate in support of increased taxes.

Courtney: I would just highlight that some of these marginally centrist politicians, like West Virginia’s [Senator] John Manchin, become incredibly important now for each specific vote. Ultimately, we don’t think it will be enough to slow the trajectory of increased deficit spending, but to Aaron’s [Dirlam] point, it’s not a mandate for any sweeping action one way or the other. We don’t think the election represented that.

Casey: For a while, I went back and forth on Biden: would he accommodate and advance the progressive policies within his party, or instead be content with just being president – kind of like Clinton – and ultimately not implement any radical changes? His track record and the number of times he’s run for president suggest the latter. But now I fear the former. I think he will actively advance – and not just get pulled into – an extremely progressive, and flat-out dangerous, agenda. I think that conclusion is supported by the ferocity by which he’s issued executive orders, the severity of those executive orders, and the goofiness of doing such things as banning the term “Wuhan virus.” But if the economy deteriorates – and I think that is a strong possibility – maybe the threat of losing mid-term elections will reign him in.

So, what legislation will advance? My fear is that they [the Democratic party] will work to cement their power by enacting long-term, institutional-type changes: make DC [the District of Columbia] and maybe Puerto Rico a state, loosen and expand voting rights, and pack the Supreme Court. Then everything else is fair game. That’s worst-case scenario. Best case is that they content themselves with typical progressive stuff: increase taxes – especially by lowering estate tax exemptions, pass a slew of environmental rules and regulations, establish some sort of universal basic income, etc.

Can they do it? John [Mauldin] is right when he mentions their power is limited by any defection of moderates from their party, but that works both ways. Can we really be confident Republicans won’t defect to their side – especially if something like universal basic income is included in a “necessary” “stimulus” bill? Please put “necessary” and “stimulus” in quotes when you publish this.

WindRock: Whether by executive order or legislation, what do you think the impact will be on energy policy? Whether it’s offshore or fracking regulations or limitations, I imagine it could be good for the price of oil, right?

Courtney: I think it’s more positive for the commodity than it is for commodity-producing equities. We still think it will be broadly positive for the [commodity- producing] equities. The best estimate I’ve seen is that most shale supply will come back on line between $65 and $70 a barrel. There’s obviously been a dramatic reduction in the amount of drilling that’s going on – specifically, in the shale patches. So, we think the market is setting up for a dramatic supply-demand imbalance in the second half of this year. That said, there are some significant developments related to work-from-home culture and what that will do to demand. It’s a little bit more nuanced than “we’re going to return to normal” and “supply is significantly lower than where it was so oil is going to the moon.”

Dirlam: Certainly, a blue sweep paves the way for lots of spending on green initiatives, but I wouldn’t run out and buy any clean energy ETF just because we don’t really know how the government is going to incentivize the green initiative. You could have some companies that just get incredible subsidies that aren’t very profitable and sort of drive down the price of for-profit entities where you’re owning the stock. That to us is an interesting area but we still need to see visibility in an infrastructure bill. We want to see some of the details of how that is going to play out before we would allocate capital to try to take advantage of that opportunity.

WindRock: Do you see any further social unrest in 2021, resembling what we had last year?

Courtney: Without a doubt. I think the burden of proof would be for anyone saying that there won’t be civil unrest. Civil unrest is not uncommon especially in economies where there’s a wide gap between income and wealth levels at the bottom and the top. I think people need to just get comfortable with the fact that this is what the landscape will look like as long as we are trying to fix the economy with monetary policy – which is an extremely blunt instrument and obviously does it in a very unequal way. So, there will be continued social decay and disruption. That’s going to lead to more violence, unfortunately, and just more frustration. I suspect a lot of people are going to get tired of watching their neighbors get rich in the middle of a prolonged recession.

Casey: I think Paul [Courtney] is totally correct. And we have timelines for this already set in stone – namely whenever the verdict comes out for [Derek] Chauvin in the death of George Floyd. But there’s also the possibility of different actors engaging in civil unrest: those against current lockdown measures. If some variant of Covid pops up and new lockdowns are enforced, will parents stand by while kids miss more school? Will loved ones continue to virtually grieve in lieu of attending a funeral? Will people stand by while friends and family are hospitalized with no hope of seeing them and advocating for them in the health care system?

WindRock: Let’s talk about the long-term effects from the lockdowns. What do you guys see as the biggest negative impact, and what could potentially benefit?

Dirlam: The biggest impact is just small businesses going under since they lacked the resources to weather the lockdowns. We had a record number of bankruptcies this past year, and record number of IPO’s. In 2020, you had all of this record corporate and high- yield bond issuance. To me those things say it all. Main Street was left behind, and Wall Street wins again. So, I think unfortunately small businesses are structurally impaired and won’t come back from this.

Mauldin: I agree, the most important economic impact will be for small business. It’s one thing to lock the door and close your small business. But you just can’t take the key, open the door, and go back to business. You’ve got to have inventory, you’ve got to have cash flow, you’ve got to have employees, and you’ve got to have capital. We will have lost thousands upon thousands of small businesses by the time we get through this. That’s a lot of workers, that’s a lot of small businesses, and they just can’t all turn back on when we reach herd immunity.

Commercial real estate is going to get repriced. We’re not going to need as much office space. I think the apartment sector will be less affected except for some urban areas – like New York City – where you have people moving to the suburbs. Just look at the U-Haul numbers. The number of people moving to Arizona, Texas, Florida, Tennessee, etc. is staggering. That’s going to affect housing from the states they’re moving out of, but it’s also going to create housing demand for the states I just mentioned. So, there’s going to be opportunities in real estate in the states that are absorbing the population.

That includes areas where it’s easy to do business or where you want to retire to. As you know, I retired to Puerto Rico, and everywhere I turn around, there’s another opportunity somewhere. We’re actually going to think about how to create a Puerto Rico fund.

Casey: I absolutely agree that small business and commercial real estate – in particular, office space in urban areas with progressive regimes like New York, LA, and Chicago – are the biggest losers. Frankly, I am shocked at how many small businesses have actually reopened, but I fear it’s a swan song for many of them. I personally know of a number of local restaurants, etc. that simply are not paying their rent. At some point, the courts will allow landlords to press their rights.