Retirement Revolution: Investment Tips From 401(k) to Roth IRA

Four Ways to Turbocharge Your Retirement Planning

Many retirement plans exist, but many of the most tax-advantageous options are often underutilized. In addition, most retirement plans fail to offer a wide range of investment options or private investment alternatives to potentially maximize growth and increase diversification. Several plans often overlooked include Solo 401k Plans, Roth IRAs, Qualified Charitable Donations, and Defined Benefit Plans. Exploring these options can help diversify your portfolio and offer even greater tax advantages.

Solo 401(k) Plans

The cornerstone of retirement planning often revolves around employer-sponsored 401(k) plans, ubiquitous among businesses of varying sizes. Yet, within this realm lies a lesser-known gem: the Solo 401(k), offering self-employed individuals and small business owners unparalleled options exceeding those of a traditional IRA.

A Solo 401(k) allows for both employer and employee contributions which effectively doubles the contribution limits compared to traditional employer-sponsored plans. This feature becomes especially attractive for self-employed individuals with a co-working spouse, as each can contribute to their respective Solo 401(k) accounts to reduce taxable income and maximize retirement savings. The chart below demonstrates the increases in contributions: 1

Solo 401(k) plans can typically be set up with the assistance of an investment adviser, by contacting the plan administrator, or by finding a different custodian. Not everyone with a 401(k) is eligible for a Solo 401(k) plan; it is specifically designed for self-employed individuals or small business owners with no full-time employees other than themselves or a spouse.

This flexibility should not only enhance returns but also provide significantly more diversification compared to standard employer-sponsored 401(k) plans with more limited investment options. Mainstream 401(k) plans typically offer a set of model portfolios based upon on a risk tolerance provided through a prompted digital questionnaire. These model portfolios often consist of only stock and bond funds, and even then seldomly sector-specific options like technology or energy. Whereas a Solo 401(k) can offer a diverse array of investment options to empower individuals to tailor their portfolios to align with their risk tolerance, market interests, and alternative investment preferences. In addition to various general and customized stock and bond funds, Solo 401(k) funds can include alternative private investments such as real estate, farmland, private equity, venture capital, precious metals, and cryptocurrencies.

Apart from a Solo 401(k), diversification can also be achieved when transitioning between employers. Upon leaving a company, rolling over a 401(k) into a traditional IRA offers greater control over investment options.

Roth IRA’s

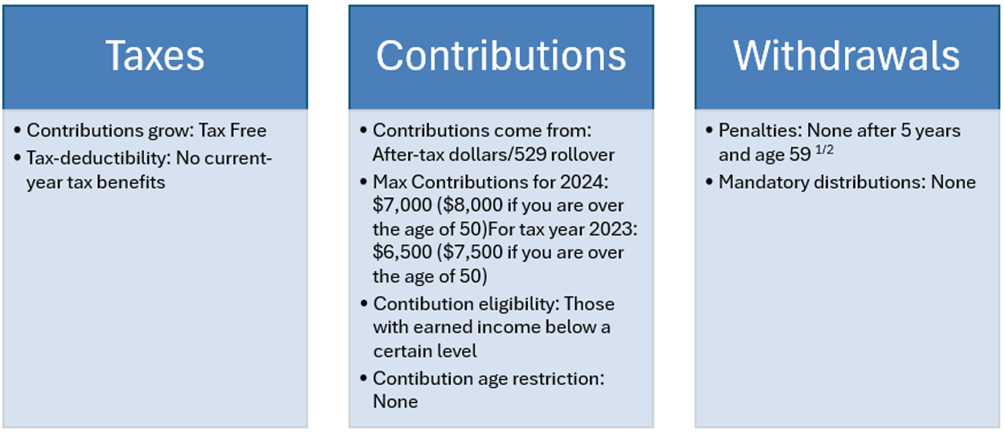

Another critical aspect to explore within 401(k) plans is the availability of a Roth component. Integrating a Roth component into a 401(k) plan can reduce tax exposure in retirement, offering both pre-tax and after-tax savings once you are of age to distribute these funds as your income. A Roth IRA, in short, grows your investment funds tax-free, but unlike a traditional IRA, allows tax-free distributions. Additionally, Roth IRAs do not require minimum distributions, enabling continued growth of savings over time and allowing greater flexibility in distribution planning. Employees can check with their administrator to see if a 401(k) Roth may be established in their plan. The following table lists the special features of Roth IRAs:

The advantages of Roth plans extend beyond the individual investor to that of their heirs. Unlike traditional 401(k)s (which are typically rolled into an heir’s 401k or IRA, thus allowing tax-free distributions only in retirement), IRA rules allow inherited Roth IRAs tax-free withdrawals in a lump-sum payment or over a ten-year period.

For individuals without access to a 401(k) Roth, Roth IRAs funded by contributions and/or conversions emerge as a powerful alternative strategy to consider at any stage of retirement planning. As Roth contributions of up to $7,000 are prohibited for investors earning more than $161,000 (single) or $240,000 (married filing jointly), Roth conversions allow an investor to circumvent these income restrictions.

A conversion involves the transfer of funds from a traditional retirement account, such as an IRA or 401(k), into a Roth account. While this triggers immediate, ordinary income taxes on the converted amount, it unlocks the potential for tax-free growth and withdrawals in retirement which is an appealing prospect for those anticipating a higher tax bracket in their golden years.

Strategically executing Roth conversions involves careful planning to manage the tax impact effectively. One approach is to spread the conversions over several years, converting smaller amounts annually. By doing so, individuals can potentially keep themselves in a lower tax bracket, mitigating the immediate tax burden while gradually transitioning their retirement savings into a tax-free vehicle. Another approach is to execute Roth conversions during years of lower income (and thus lower tax rates) or financial market downturns (so asset values, and thus taxes, are reduced).

For individuals unable to contribute to Roth plans given their income levels, funding (apart from a conversion) can still be achieved with a backdoor Roth strategy. Here, investors fund an IRA with the annual contribution amount and then transfer it to a Roth IRA. To avoid tax implications, be sure to claim the IRA contribution as a non-deductible contribution and transfer from a zero-balance IRA to your Roth.

No matter how old or how much income you earn, Roth IRAs can be an option for you.

Qualified Charitable Contributions

Another retirement planning strategy uses Qualified Charitable Distributions (QCDs) from their IRAs allowing retirees aged 70 and a half or older to support charitable causes.

With QCDs, individuals directly transfer funds from their IRA to a qualified charity for up to $100,000 a year without triggering tax implications. This provision proves particularly advantageous for retirees subject to Required Minimum Distributions (RMDs) but who may not require or desire the entirety of their distributions.

Integrating QCDs with Roth conversions presents a compelling synergy, unlocking dual benefits for retirees. By directing RMDs to charitable organizations and subsequently executing Roth conversions with other retirement funds, individuals can effectively reduce their taxable income while expediting the transition to tax-free Roth accounts. This strategic maneuver not only benefits charitable causes but also enhances the overall tax efficiency of retirement savings.

Business owners can also leverage the power of QCDs to mitigate tax liabilities while supporting charitable endeavors. By combining a QCD with a company charitable donation, business owners can potentially cover a significant portion, if not the entire, tax liability. For example, if a business owner had $500k in an IRA and they wished to convert most of it to a Roth, the tax liability could be reduced to zero by both using the $100k QCD allotment and making a tax-deductible business expense equal to the conversion’s tax liability. The business deduction will then flow through to the owner to offset the tax liability associated with the $400k remaining conversion.

However, navigating the intricacies of QCDs requires meticulous adherence to IRS guidelines to qualify for the associated tax benefits. Working closely with tax professionals and charitable advisors can provide invaluable guidance in executing this strategy effectively and maximizing its impact within a comprehensive retirement plan.

By understanding and leveraging QCDs in conjunction with Roth conversions, individuals can ensure a secure and impactful retirement while leaving a legacy in support of causes close to their hearts.

Defined Benefit Plans

For high-earning professionals and business owners crafting their retirement strategy, the inclusion of a defined benefit plan emerges as a pivotal consideration. These plans, often referred to as pension plans, represent a potent vehicle for accumulating substantial tax-deferred contributions towards retirement savings.

Unlike defined contribution plans such as 401(k)s or IRAs, which are bound by annual contribution limits, defined benefit plans offer unparalleled flexibility. Individuals can contribute amounts tailored to fund a specific retirement benefit, allowing for strategic optimization of savings in alignment with personal financial goals. Defined benefit plans are created to provide annual contribution flexibility. Defined benefit plans incorporate an eventual monetary benefit objective at the end of a specified term. For example, an investor may have a 10-year term to reach a $1,000,000 benefit. If $200,000 is contributed for the first three years, then several (or more) future years may not require any contribution if the third-party administrator (TPA) determines the contributions (and their expected returns) are “on track” per IRA guidelines to meet the eventual benefit. Businesses with profit cyclicality may find this contribution flexibility appealing.

The maximum contribution to a defined benefit plan hinges on various factors, including age, expected retirement age, and desired retirement benefit, but can often allow contributions of several hundred thousand dollars per year. A few TPAs will even include a life insurance component to maximize deductions and increase contributions even more.

However, establishing and managing a defined benefit plan involves considerable complexity, often requiring expert guidance. Third-party administrator firms conduct in-depth analyses of employee ages, compensation, and tenure to determine if pursuing such a plan is worthwhile. Defined benefit plans also necessitate timely management and require an oversight administrator (separate from the financial advisor) along with a TPA and a CPA to ensure ongoing compliance.

Conclusion

Solo 401(k) plans, Roth IRAs, Qualified Charitable Distributions (QCDs), and defined benefit plans each offer unique benefits and opportunities for individuals to optimize their retirement savings and tax efficiencies. In addition, these retirement vehicles allow investors to avail themselves of private offerings typically unavailable in traditional vehicles like 401(k)s. Private investments such as precious metals, private credit, cryptocurrencies, real estate, private equity, etc. may facilitate more sophisticated and diversified investment portfolios with potentially better risk/return profiles than the traditional stock and bond paradigm.

Investors should understand and consider these underutilized planning techniques and vehicles to pave the way for a comfortable and fulfilling retirement while leaving a legacy for future generations.

Endnotes:

- IRS.gov – this footnote applies to the remainder of the article

- “Roth vs. Traditional.’ Schwab Brokerage, www.schwab.com/ira/roth-vs-traditional-ira.

About WindRock

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high-net-worth individuals, family offices, foundations and retirement plans.

Adding Austrian Economics

The following is a transcript of a speech by Christopher Casey of WindRock Wealth Management to the Mises Institute’s 2016 Supporters Summit held on September 17th in Asheville, North Carolina.

In thinking about the title of this presentation, it occurred to me that some people may be uninterested. That is, attendees may feel they manage their own investments, and are therefore unthreatened by wealth managers ignorant of Austrian economics.

Fortunately, in the last several weeks, we have learned that a certain major bank has been kind enough to open multiple accounts for each and every person in this room.

So, it turns out you actually are at risk. We are living in a distinctive time period, which has introduced terms as unique as they are dangerous. Terms like negative interest rates, excess reserve balances, and quantitative easing.

I wish I could say we live in unparalleled times, and it is true that this economic situation is unique, but there are parallels in the magnitude of its gravity. Dates like 1928 and 2007 come to mind.

And no election will bring relief: we are faced with the choice between a man who frequently displays errors of judgement and a woman whose judgement is consistently in error.

I do not need to remind this audience of the worldwide economic situation that threatens the livelihoods of billions. But there is another danger lurking. One that threatens billions in savings. Actually, trillions. As Jeff Deist noted last night, the economics profession is broken. The same can be said for the wealth management industry. But while government officials, crony capitalists, and to a large degree, mainstream economists are motived by greed and power, the beliefs of wealth managers are driven by cowardice and ignorance. And this is evident from every phrase they utter.

The cowardice is evident from their 2009 chorus of “no one saw this coming” to their mantra of “you can’t time the market.”

The ignorance is apparent when they use phrases such as an “overheated economy.”

So, allow me to review some of the mistaken beliefs held by wealth managers, and how it impacts one’s portfolio.

First, price inflation. A word which used to be feared, but now is strangely welcomed by government officials.

Wealth managers speak of it even less than they understand it. They may have some vague understanding that it has something to do with the quantity of dollars which exist. They probably learned a phrase from a famous but flawed economist that:

“Inflation is always and everywhere a monetary phenomenon.”

But what does that really mean? It’s like saying ice and snow are always an everywhere a temperature phenomenon.

It doesn’t tell us much, because the statement’s truth is as selfWevident as it is incomplete.

Despite the massive increase in the money supply, wealth managers are unconcerned about inflation. They believe that, as long as wage and cost pressures are manageable, the economy will not “overheat.”

For the record, the ONLY thing on this earth less likely to become overheated than an economy . . . is someone trying to hide a serious illness while running for President.

If you ask a wealth manager what they mean by “overheating”, most cannot answer the question. Analogies are great to illustrate concepts, but this analogy has replaced the concept itself.

What they are trying to articulate is the classic theory of “demandWpull” inflation. It is the belief that until high employment levels and high factory utilization are achieved, prices will not rise.

Recessions and weak economic growth preclude inflation because aggregate demand, whatever that is, fails to increase substantially.

But apparently, no wealth manager lived through the 1970’s, because that’s exactly what we had.

They also do not fear inflation because commodity prices such as oil and agricultural products are low. In their paradigm, inflation occurs when costs rise and ultimately bubble up to consumer prices.

But if the price of oil or some other costWpush culprit rises, the buyers have less money to spend on other goods and services. Having less money to purchase something means less demand exists, and decreased demand reduces prices.

So, while some prices go up, it is at the expense of other prices which go down. Ultimately, no net effect to the overall price level.

We can see this with their false villain for the price inflation of the 1970’s: oil. The oil price increase in the 1970’s was certainly dramatic, but the price of oil has experienced equally pronounced changes in prices over the last decade or so as well.

Has the overall price level changed accordingly? Has the

U.S. economy experienced significant inflation and deflation as oil moved from $25 in April 2003 up to $133 in July 2008, down to $40 in December 2008, back up to $125 in March 2012, and down to less than $30 earlier this year?

Does anyone remember the price level gyrating like that over the last decade or so?

As if these misconceptions by wealth managers are not enough, they also do not believe we will have inflation as long as the “velocity” of money stays low.

I find this belief particularly odd. How can dollars independently create prices without the goods or services with which they transact?

The idea of velocity derives from an equation popularized in the early part of the 20th century by the economist Irving Fisher to explain the price level. But it originally derived from, of all people, Copernicus. However, while he was correct about that Sun thing, he was wrong about this.

The flaw is that velocity is not a proxy for the demand for money. If anything, maybe we can say it represents volume. And the volume of transactions has no bearing on prices. Strange that wealth managers do not apply their velocity theory to the stock market: they talk about weak or high volume, but no one says weak or high volume causes stock indices to move up or down.

Austrian economic theory proposes that money, like any other good, has a price set by supply and demand. So, any theory of a price level – which is another way of saying a theory of the value of money – which ignores demand is flawed.

If wealth managers really think low monetary velocity is keeping a lid on inflation, they will be surprised when inflation eventually skyrockets despite low velocity.

So not only do wealth managers fail to prepare portfolios for any possible inflation, but the concept of inflation is so alien to them, they neglect to convey its effects when determining investment returns.

Wealth managers are equally unable to explain recessions.

All of us are familiar with the basic outline of Austrian business cycle theory: artificial increases in the money supply lowers interest rates below their natural levels which induces economic actors to make malinvestments which are ultimately revealed in a recession.

A few wealth managers may subscribe to a Chicago school or Keynesian business cycle theory, but many believe recessions are natural outgrowths of the free market and are, in fact, unexplainable.

They cannot explain the widespread and severely erroneous judgment of businesses in forecasting the future as revealed in the “bust”.

They cannot explain why it is a cycle, and why this cycle first appeared in the 19th century.

They cannot explain why capital goods industries are more sensitive to booms and busts relative to consumer goods industries.

They cannot explain why significant money supply expansion precedes every single recession. But the wealth management industry’s ignorance about the causation of business cycles is surpassed by their misunderstanding of recession remedies.

As Austrians, we know one directive should be followed by policy makers in a recession: do not interfere with the economy’s adjustment process.

Do not prevent the liquidation of assets or companies with bailouts. Do not stimulate consumption and discourage savings through deficits and other means. And above all, do not inflate the money supply again which will only bring another recession in the future.

Because wealth managers do not have an adequate theory of what causes recessions, they applaud the standard recipe used to deal with economic downturns: big bailouts, huge deficits, and massive monetary expansion.

It is to the point now where they buy stocks and bonds solely in reaction to Federal Reserve action. Or better stated, inaction.

It is to the point now where the interpretation of Federal Reserve policy is as delicate and important a science as that of the Kremlinologists from days past.

Who is standing next to whom at the May Day parade has been replaced by which words have been added or deleted from the minutes of meetings.

Not only do the stock and bond markets move solely in relation to the Federal Reserve, but the Federal Reserve acts only in relation to the stock market. It’s like they’ve formed some sort of binary black hole system.

A key reason why wealth managers applaud dovish Federal Reserve comments and actions, and a key reason why the Federal Reserve acts as such, is the mistaken believe in the “wealth effect”.

They believe that by increasing wealth through rising stock and housing prices, the populace will increase their consumer spending which will spur economic growth.

Regardless as to whether or not increased wealth will actually spur increased consumer spending, the most important component of the wealth effect is the assumption that increased consumer spending stimulates economic growth.

It is a pure Keynesian concept and it is critical to the wealth effect’s validity. If increased consumer spending fails to stimulate the economy, the theory of the wealth effect fails. Wealth effect turns, in effect, into wealth defect.

Does increased consumer spending improve the economy? On one side of the argument, we have the aggregate individual conclusions of hundreds of millions of economic actors, each acting in their own best interest. These individuals and businesses are attempting to reduce consumer spending and increase savings.

Dissenting from their views is Board of Governors of the Federal Reserve. Each member appears to believe in the paradox of thrift – the belief that increased savings, while beneficial for any particular economic actor, have negative effects for the economy as a whole.

The paradox of thrift can essentially be described as this: decreased consumer spending lowers aggregate demand which reduces employment levels which negatively affects consumption which in turn lowers aggregate demand. The paradox predicts an economic death spiral from diminished demand.

But history suggests the opposite: it is higher savings rates which lead to economic prosperity. Examine any economic success story such modern China, 19th century America, or postWWorld War II Japan and South Korea: did their economic rise derive from unbridled consumption, or strict frugality?

The answer is selfWevident: it is the savings from the curtailment of consumption, combined with minimal government involvement in economic affairs, which generates economic growth.

So why do so many wealth managers and economists falsely believe in the paradox of thrift, and thus the wealth effect? It is because of their mistaken understanding of the nature of savings. They believe savings leak out of the economic system and are never spent.

But savings are indeed spent. Not directly by consumers on electronics and espressos, but indirectly by businesses via banks on more efficient machinery and capital expansions. Increased savings may (initially) negatively affect retail shops, but it benefits producers which create the goods demanded from the increased pool of savings. On the whole, the economy is more efficient and prosperous. So, to what investment advice do these economic fallacies lead? What errors are being inflicted upon one’s portfolio?

Without fear of either inflation or recessions, wealth managers have no understanding of interest rates, and thus see no danger in bonds.

It is somewhat understandable. Given the recent history of massive intervention in the bond markets by central banks, few remember that interest rates are ultimately a product of the free market.

At a fundamental level, interest rates reflect the time preferences of various actors within the economy. Add in assessments of credit risk as well as expectations of future price levels, and a structure of interest rates over various time frames is revealed.

All markets can be suppressed, distorted, or manipulated, but only for a limited time. The bond market is no different; whether through a sober assessment of credit worthiness by investors or via rising price inflation, the market will compel higher interest rates.

For this reason, the U.S. government has suppressed interest rates for years: it simply cannot afford for them to rise. It will continue to do so by remaining reliant (and increasingly so) upon the printing press to purchase bonds to lower rates. But this strategy will only work for so long.

In Human Action, Mises wrote:

Nobody believes that the states will eternally drag the burden of these interest payments. It is obvious that sooner or later all these debts will be liquidated in some way or other, but certainly not by payment of interest and principal according to the terms of the contract.

If the Federal Reserve continues with proliferate production runs of the printing presses, expect Mises to be prophetic: bondholders will be “repaid”, but with a currency which hardly meets the “terms of the contract.”

Wealth management’s enthusiasm for stocks and bonds is matched only by their hostility to such inflationary recession protections as precious metals, private lending, and certain types of real estate such as farmland and rental residential properties.

The hostility to gold can be seen by its widespread exclusion from recommend investment allocations. It can be seen by the fact that the value of all of the gold in the world ever mined is dwarfed by the national debt of the U.S. It can be seen by the fact the entire gold mining industry is easily dwarfed in value by a number of individual U.S. stocks.

The fact advisors ignore such major asset classes as farmland is a great example of the problems with the wealth management industry. For even if they heeded the dangers of inflation and recessions, they could not consider farmland within their portfolios.

The reason is that there are very few public farmland vehicles – Real Estate Investment Trusts – or REITs, in the

U.S. Accordingly, there are no investment benchmarks for farmland to be considered by wealth advisors (because the sample size is too small).

Therefore, wealth advisory firms will not consider an investment in farmland. Mind you, it’s not because the investment opportunity doesn’t exist, rather it is because wealth managers cannot be viewed as performing out of sync with commonly used real estate investment benchmarks. To do otherwise will entail risking their careers.

This is the real problem in the wealth advisory industry – advisors are worried about losing clients, not with losing clients’ money. Wealth advisors are happy tracking what everyone else is doing – because in so doing, they believe they are preventing their clients from switching to another firm. This “career risk” syndrome forces wealth advisors into shortWterm outlooks and a herdWlike mentality.

Wealth managers really manage money, not wealth. Wealth is beyond that of money and includes such things as health, judgement, and knowledge – basically everything that helps bring about our happiness.

But money is a critical component. It grants optionality and the means to make choices.

Mises understood this and embodied it in the concept of acting man – the motivation to increase one’s level of satisfaction.

The best way to maximize your satisfaction Wyour wealthW is to make sure your portfolio is guided by Austrian economic theory.

Christopher P. Casey is a Managing Director with WindRock Wealth Management. Mr. Casey advises clients on their investment portfolios in today’s world of significant economic and financial intervention. He can be reached at 312O650O9602 or chris.casey@windrockwealth.com.

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high net worth individuals, family offices, foundations and retirement plans.

All content and matters discussed are for information purposes only. Opinions expressed are solely those of WindRock Wealth Management LLC and our staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. FeeWbased investment advisory services are offered by WindRock Wealth Management LLC, an SECW Registered Investment Advisor. The presence of the information contained herein shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services except, where applicable, in states where we are registered or where an exemption or exclusion from such registration exists. WindRock Wealth Management may have a material interest in some or all of the investment topics discussed. Nothing should be interpreted to state or imply that past results are an indication of future performance. There are no warranties, expresses or implied, as to accuracy, completeness or results obtained from any information contained herein. You may not modify this content for any other purposes without express written consent.

Problems with Today’s Wealth Management Industry

Christopher P. Casey

Question: Although WindRock Wealth Management is a U.S.-based Registered Investment Advisor which manages money for wealthy individuals, you certainly seem different from other firms out there. One of those differences is your macroeconomic viewpoints. Why is that important to WindRock?

WindRock: It is amazing but true, many wealth advisory firms have no view on the economy! I cannot tell you how many times I have asked Chief Investment Officers of major wealth advisory firms what causes recessions, and their response is either “we don’t know” or “we’re agnostic as to the economy” – whatever that means. If any firms hold any views on the economy, they typically adhere to Keynesian economics – they basically just parrot what the Federal Reserve and other mainstream organizations predict. And the Federal Reserve in particular has a horrific track record in this regard – having not only completely missed the 2008 recession and the 2007 housing crisis, but also by initially dismissing the impact of Covid on the economy.

So, we think having a well-thought-out view on the economy is a tremendous advantage. We think it’s important in designing portfolios. In particular, we favor the Austrian school of economics which is an alternative to Keynesian philosophy. Austrian economists, unlike the mainstream Keynesian economists, understand what truly causes inflation and recessions – the artificial expansion of the money supply by central banks. Since these are the two greatest threats to anyone’s investment portfolio, this understanding is critical. This is why many wealth advisory firms herded their clients right over the cliff with the crash in technology stocks and later with all equities in 2008 – which we can see repeating in the future. They could not foresee these events because those events don’t comport to their flawed models and theories. For the same reason, they do not foresee any danger with today’s overvalued U.S. stock and bond markets. By using Austrian economics, we have a time-tested tool to guide our decisions.

Question: Recessions pop asset valuations, and are thus a threat to anyone’s portfolio, but what about inflation? What do you see going forward and how do you position clients accordingly?

WindRock: The actions of the Federal Reserve since August 2008 – and especially since March 2020 – are truly unprecedented. Depending on how you measure it, the U.S. money supply has increased over 75% since the lockdowns were initiated. We’re at historically high year-over-year growth rates – and we have been since March 2020. Increasing the money supply to this degree will inevitably cause significant inflation. It may not show up soon, it may even be preceded by some brief deflation – although I doubt that, but it will develop. When this happens, stocks will, at best, be flat in real terms. And bonds will be decimated. The only way to protect one’s wealth is to invest in such thing as precious metals, cryptocurrencies like bitcoin, and certain types of real estate – mainly farmland and rental residential real estate in the Sun Belt states. Positioning one’s portfolio as such will not only offer protection, but great profit. And this isn’t just based in theory, but in experience. The historical performance of these investments in the 1970’s in America offers great guidance – while the price index more than doubled in 10 years, farmland and gold provided tremendous appreciation.

Question: How do you design portfolios?

WindRock: Our clients’ risk profiles and liquidity needs are integrated with our projections of real economic growth and price levels over the next twelve months. We then combine this with our judgment as to overall asset valuations in the equity and debt markets to determine the allocation between stocks, bonds, and hard assets such as real estate and precious metals. After determining these broad allocations, those same assessments dictate the constituent parts of each allocation. For example, if we are in equities, how much is in emerging markets versus the developed world? How much is defensive versus aggressive, etc.?

One additional item I should note about portfolio construction, we do not believe in “putting all of your chips on red” and waiting for the big payoff. By that I mean we select investments we expect to do very well when the economy plays out the way we expect, but they will also do well in the interim due to the compelling risk and return profile the investment itself offers. As an example, we believe multi-family rental real estate will do quite well in the U.S. when a housing decline unfolds due to rising interest rates and/or inflation hits. Our play has been to focus on new construction neighborhoods that rent like apartments but look and feel like single family homes. We did not go out and buy a publicly traded rental real estate vehicle – they are currently overvalued – which may do well in a housing decline and/or with inflation – we found an investment which believe will do well regardless since it is building a new type of multi-family housing community.

Question: What else differentiates WindRock from other wealth advisory firms?

WindRock: It’s not just about having a different view on how economies work. It’s about what you do with that knowledge. It’s about having an entrepreneurial mindset to act on these opportunities – to seek out and vet investment vehicles which the mainstream wealth advisory industry won’t touch. I think we describe this well on our website where we wrote:

Conventional wisdom associates the word “entrepreneur” with the assumption of risk. While risk can never be fully avoided, what actually makes entrepreneurs unique is their understanding of risk. Our unique insight of the risks posed by governmental interference in the economy serves to protect our clients’ wealth. As entrepreneurial-minded advisors, we emphasize independent and creative thought to boldly seize opportunities while minimizing key risks.

Farmland is a great example. There are very few public farmland vehicles – Real Estate Investment Trusts – or REITs, in the U.S. Accordingly, there are no investment benchmarks for farmland to be considered by mainstream wealth advisors (because the sample size is too small). Therefore, mainstream wealth advisory firms will not consider an investment in farmland. Mind you, it’s not because the investment opportunity isn’t there, but because they cannot be viewed as performing out of sync with the commonly used real estate investment benchmarks. To do otherwise will entail risking their careers. This is a real problem in the wealth advisory industry – advisors are worried about losing clients, not with losing clients’ money. The mainstream wealth advisors are happy tracking what everyone else is doing – because in so doing, they believe they are preventing their clients from switching to another firm. This “career risk” syndrome forces wealth advisors into short-term outlooks with a herd-like mentality.

This is a real problem in the wealth advisory industry – advisors are worried about losing clients, not with losing clients’ money.

Question: Besides the lack of an economic viewpoint (or an incorrect one), besides the “career risk” mentality, what other problems exist within the wealth advisory industry?

WindRock: Misaligned incentives. Many firms lack independence, meaning they create and market their own investment vehicles. So oftentimes they’re not just advising clients to own a particular type of investment – they’re advising clients to own their investment. Which certainly means additional fees and probably a sub- performing investment vehicle. I cannot tell you how many times I have reviewed a prospective client’s investments only to find they are heavily invested in their advisor’s funds. Is it really that likely that the best emerging market equity fund just happens to be owned and run by the advisor’s firm? That the very same advisory firm has the top currency fund? What are the odds?

Question: So, the XYZ Wealth Management firm owns the XYZ funds . . .

WindRock: I think common sense and anecdotal evidence suggests that if you examined client statements from all wealth advisory firms, you will not find the ownership dispersion you would expect if wealth advisors truly provided independent advice. This Wall Street sales culture permeates many firms. Unfortunately, the more wealth advisors serve as salesmen, the less they act as a trusted advisor.

Question: With all of these problems in the industry, why should investors even consider using a wealth advisor?

Unfortunately, the more wealth advisors serve as salesmen, the less they act as a trusted advisor.

WindRock: Doing it yourself can be an option. And perhaps a fairly viable one when compared to the alternative of using many of these firms. But there are still compelling reasons to use a wealth advisory firm. For example, since wealth advisors possess buying power by representing numerous clients, we can have access to certain investment vehicles which may simply be unavailable to the individual investor. In addition, we can negotiate lower fees and minimum investments with the funds we utilize. But in a greater context, maximizing returns and minimizing risks for any investment portfolio requires time, research, money, judgement, and knowledge. It’s a full-time job, especially in today’s world of massive government intervention in the economy and the financial markets, to manage a portfolio. This is why we created WindRock, because wealth advisory has its place – it just needs a different economic viewpoint, a unique investing mindset, and greater independence.

Question: How can anyone interested contact you to learn more about WindRock’s services?

WindRock: Of far greater importance than what we do is what we believe. All of our marketing is driven by thought-leadership, so I encourage any interested parties to visit our webpage at www.windrockwealth.com to read about our philosophy as well as our regularly posted research and analysis. I also suggest interested parties to sign up for our mailing list.

About WindRock

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high-net-worth individuals, family offices, foundations and retirement plans.

312-650-9602

Why Economics Should Guide Investment Allocations

Jeff Deist, President of the Mises Institute, interviews Christopher Casey. Topics include why economics should guide investment allocations; why adherence to the Austrian school of economics is growing within the finance community; how inflation can erode investment returns and capital; why Federal Reserve and other government officials are consistently wrong in their economic outlooks; what investments can protect investors in an inflationary environment; and where the housing market may be headed. November 2014.