Many retirement plans exist, but many of the most tax-advantageous options are often underutilized. In addition, most retirement plans fail to offer a wide range of investment options or private investment alternatives to potentially maximize growth and increase diversification. Several plans often overlooked include Solo 401k Plans, Roth IRAs, Qualified Charitable Donations, and Defined Benefit Plans. Exploring these options can help diversify your portfolio and offer even greater tax advantages.

Solo 401(k) Plans

The cornerstone of retirement planning often revolves around employer-sponsored 401(k) plans, ubiquitous among businesses of varying sizes. Yet, within this realm lies a lesser-known gem: the Solo 401(k), offering self-employed individuals and small business owners unparalleled options exceeding those of a traditional IRA.

A Solo 401(k) allows for both employer and employee contributions which effectively doubles the contribution limits compared to traditional employer-sponsored plans. This feature becomes especially attractive for self-employed individuals with a co-working spouse, as each can contribute to their respective Solo 401(k) accounts to reduce taxable income and maximize retirement savings. The chart below demonstrates the increases in contributions: 1

Solo 401(k) plans can typically be set up with the assistance of an investment adviser, by contacting the plan administrator, or by finding a different custodian. Not everyone with a 401(k) is eligible for a Solo 401(k) plan; it is specifically designed for self-employed individuals or small business owners with no full-time employees other than themselves or a spouse.

This flexibility should not only enhance returns but also provide significantly more diversification compared to standard employer-sponsored 401(k) plans with more limited investment options. Mainstream 401(k) plans typically offer a set of model portfolios based upon on a risk tolerance provided through a prompted digital questionnaire. These model portfolios often consist of only stock and bond funds, and even then seldomly sector-specific options like technology or energy. Whereas a Solo 401(k) can offer a diverse array of investment options to empower individuals to tailor their portfolios to align with their risk tolerance, market interests, and alternative investment preferences. In addition to various general and customized stock and bond funds, Solo 401(k) funds can include alternative private investments such as real estate, farmland, private equity, venture capital, precious metals, and cryptocurrencies.

Apart from a Solo 401(k), diversification can also be achieved when transitioning between employers. Upon leaving a company, rolling over a 401(k) into a traditional IRA offers greater control over investment options.

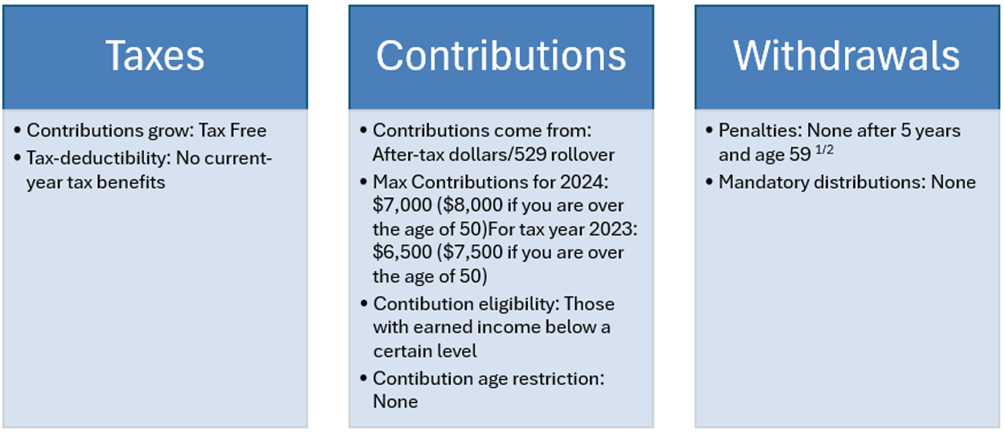

Roth IRA’s

Another critical aspect to explore within 401(k) plans is the availability of a Roth component. Integrating a Roth component into a 401(k) plan can reduce tax exposure in retirement, offering both pre-tax and after-tax savings once you are of age to distribute these funds as your income. A Roth IRA, in short, grows your investment funds tax-free, but unlike a traditional IRA, allows tax-free distributions. Additionally, Roth IRAs do not require minimum distributions, enabling continued growth of savings over time and allowing greater flexibility in distribution planning. Employees can check with their administrator to see if a 401(k) Roth may be established in their plan. The following table lists the special features of Roth IRAs:

The advantages of Roth plans extend beyond the individual investor to that of their heirs. Unlike traditional 401(k)s (which are typically rolled into an heir’s 401k or IRA, thus allowing tax-free distributions only in retirement), IRA rules allow inherited Roth IRAs tax-free withdrawals in a lump-sum payment or over a ten-year period.

For individuals without access to a 401(k) Roth, Roth IRAs funded by contributions and/or conversions emerge as a powerful alternative strategy to consider at any stage of retirement planning. As Roth contributions of up to $7,000 are prohibited for investors earning more than $161,000 (single) or $240,000 (married filing jointly), Roth conversions allow an investor to circumvent these income restrictions.

A conversion involves the transfer of funds from a traditional retirement account, such as an IRA or 401(k), into a Roth account. While this triggers immediate, ordinary income taxes on the converted amount, it unlocks the potential for tax-free growth and withdrawals in retirement which is an appealing prospect for those anticipating a higher tax bracket in their golden years.

Strategically executing Roth conversions involves careful planning to manage the tax impact effectively. One approach is to spread the conversions over several years, converting smaller amounts annually. By doing so, individuals can potentially keep themselves in a lower tax bracket, mitigating the immediate tax burden while gradually transitioning their retirement savings into a tax-free vehicle. Another approach is to execute Roth conversions during years of lower income (and thus lower tax rates) or financial market downturns (so asset values, and thus taxes, are reduced).

For individuals unable to contribute to Roth plans given their income levels, funding (apart from a conversion) can still be achieved with a backdoor Roth strategy. Here, investors fund an IRA with the annual contribution amount and then transfer it to a Roth IRA. To avoid tax implications, be sure to claim the IRA contribution as a non-deductible contribution and transfer from a zero-balance IRA to your Roth.

No matter how old or how much income you earn, Roth IRAs can be an option for you.

Qualified Charitable Contributions

Another retirement planning strategy uses Qualified Charitable Distributions (QCDs) from their IRAs allowing retirees aged 70 and a half or older to support charitable causes.

With QCDs, individuals directly transfer funds from their IRA to a qualified charity for up to $100,000 a year without triggering tax implications. This provision proves particularly advantageous for retirees subject to Required Minimum Distributions (RMDs) but who may not require or desire the entirety of their distributions.

Integrating QCDs with Roth conversions presents a compelling synergy, unlocking dual benefits for retirees. By directing RMDs to charitable organizations and subsequently executing Roth conversions with other retirement funds, individuals can effectively reduce their taxable income while expediting the transition to tax-free Roth accounts. This strategic maneuver not only benefits charitable causes but also enhances the overall tax efficiency of retirement savings.

Business owners can also leverage the power of QCDs to mitigate tax liabilities while supporting charitable endeavors. By combining a QCD with a company charitable donation, business owners can potentially cover a significant portion, if not the entire, tax liability. For example, if a business owner had $500k in an IRA and they wished to convert most of it to a Roth, the tax liability could be reduced to zero by both using the $100k QCD allotment and making a tax-deductible business expense equal to the conversion’s tax liability. The business deduction will then flow through to the owner to offset the tax liability associated with the $400k remaining conversion.

However, navigating the intricacies of QCDs requires meticulous adherence to IRS guidelines to qualify for the associated tax benefits. Working closely with tax professionals and charitable advisors can provide invaluable guidance in executing this strategy effectively and maximizing its impact within a comprehensive retirement plan.

By understanding and leveraging QCDs in conjunction with Roth conversions, individuals can ensure a secure and impactful retirement while leaving a legacy in support of causes close to their hearts.

Defined Benefit Plans

For high-earning professionals and business owners crafting their retirement strategy, the inclusion of a defined benefit plan emerges as a pivotal consideration. These plans, often referred to as pension plans, represent a potent vehicle for accumulating substantial tax-deferred contributions towards retirement savings.

Unlike defined contribution plans such as 401(k)s or IRAs, which are bound by annual contribution limits, defined benefit plans offer unparalleled flexibility. Individuals can contribute amounts tailored to fund a specific retirement benefit, allowing for strategic optimization of savings in alignment with personal financial goals. Defined benefit plans are created to provide annual contribution flexibility. Defined benefit plans incorporate an eventual monetary benefit objective at the end of a specified term. For example, an investor may have a 10-year term to reach a $1,000,000 benefit. If $200,000 is contributed for the first three years, then several (or more) future years may not require any contribution if the third-party administrator (TPA) determines the contributions (and their expected returns) are “on track” per IRA guidelines to meet the eventual benefit. Businesses with profit cyclicality may find this contribution flexibility appealing.

The maximum contribution to a defined benefit plan hinges on various factors, including age, expected retirement age, and desired retirement benefit, but can often allow contributions of several hundred thousand dollars per year. A few TPAs will even include a life insurance component to maximize deductions and increase contributions even more.

However, establishing and managing a defined benefit plan involves considerable complexity, often requiring expert guidance. Third-party administrator firms conduct in-depth analyses of employee ages, compensation, and tenure to determine if pursuing such a plan is worthwhile. Defined benefit plans also necessitate timely management and require an oversight administrator (separate from the financial advisor) along with a TPA and a CPA to ensure ongoing compliance.

Conclusion

Solo 401(k) plans, Roth IRAs, Qualified Charitable Distributions (QCDs), and defined benefit plans each offer unique benefits and opportunities for individuals to optimize their retirement savings and tax efficiencies. In addition, these retirement vehicles allow investors to avail themselves of private offerings typically unavailable in traditional vehicles like 401(k)s. Private investments such as precious metals, private credit, cryptocurrencies, real estate, private equity, etc. may facilitate more sophisticated and diversified investment portfolios with potentially better risk/return profiles than the traditional stock and bond paradigm.

Investors should understand and consider these underutilized planning techniques and vehicles to pave the way for a comfortable and fulfilling retirement while leaving a legacy for future generations.

Endnotes:

- IRS.gov – this footnote applies to the remainder of the article

- “Roth vs. Traditional.’ Schwab Brokerage, www.schwab.com/ira/roth-vs-traditional-ira.

About WindRock

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. We serve as the trusted voice to a select group of high-net-worth individuals, family offices, foundations and retirement plans.